Loans and guarantees are naturally paired. They both aim to channel preferential credit to firms, with the government bearing the risk. In a loan programme, governments lend directly. In a guarantee scheme, they underwrite risks assumed by banks. The economic logic is the same. Only the institutional arrangement differs. For this piece of GTA’s State Capitalism series, we examined 596 guarantee and 1’783 loan programmes announced during 2009-2025.

The Pandemic Legacy in State Credit

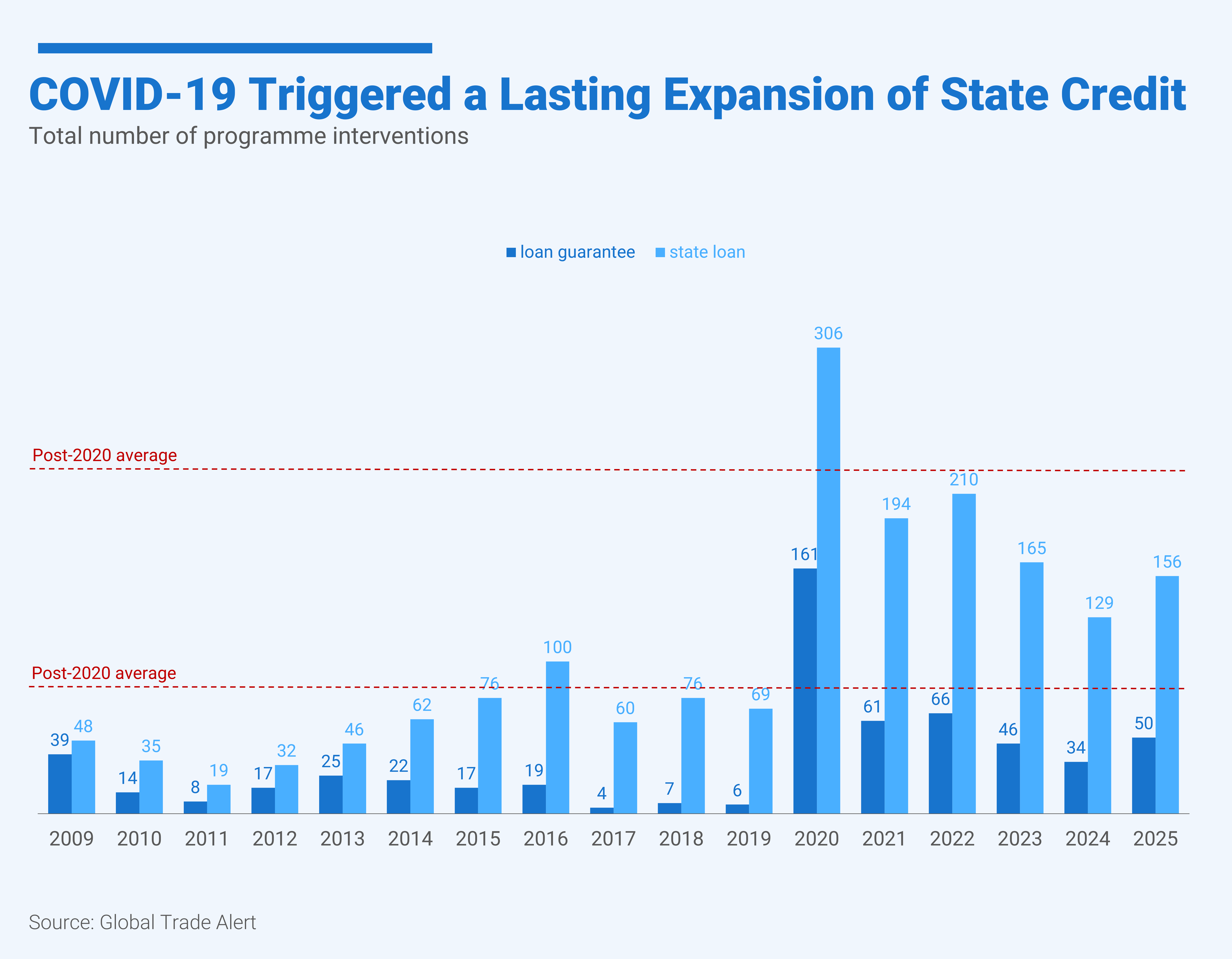

Credit programmes peaked in 2020, and their expansion proved lasting. New guarantee programmes peaked at 161 in 2020, and loan programmes reached 306. Since 2021, they have averaged three times their pre-pandemic levels. On average, 222 new programmes emerged worldwide each year from 2021 to 2025, compared with 73 during 2009–2019.

Strict sectoral targeting faded with the pandemic and has not reversed since. Between 2009 and 2019, sector-specific programmes consistently dominated public credit, accounting for 55% to 93% of all. The pandemic broke that pattern. In 2020, horizontal programmes (i.e. those open to all economic sectors) represented 62% of the total. This was also the first and only time economy-wide support constituted a majority on record. While that peak has since moderated, the shift has proven durable: appetite for economy-wide lending support has permanently widened.

This shift does not, however, imply unconditional access. Many horizontal programmes remain tied to specific objectives rather than open to any use. Green transition, innovation, and digitalisation feature prominently as qualifying criteria. The EU’s flagship InvestEU Programme, for instance, channels USD 30.9 billion (at the time of issuance) over the 2021-2027 period for projects related to strategic investments, green and digital transitions, enhanced resilience and strengthening strategic value chains. Similar thematic targeting appears elsewhere, including South Korea’s USD 313.8 billion pledge to support companies adopting low-carbon conversion and energy transition projects and India’s USD 11.7 billion Research Development and Innovation Scheme.

Who Uses State Credit the Most

The geography of state credit is heavily concentrated. The top ten implementors[1] account for 84% of the recorded total.

The EU and its Member States account for 1’044 programmes, almost one in every two recorded on the site. Two factors explain this. First, the Commission announced two broad state aid frameworks to streamline financial support to companies following the COVID-19 pandemic and the Russian invasion of Ukraine. Under these frameworks, 296 state aid schemes, including loans and guarantees, were approved across the Union since 2020. Second, the EU centralised state aid register offers the closest thing to a comprehensive disclosure system and it captures activity across all Member States. Italy (192), France (145), Spain (117) and Germany (107) led the way. Half the schemes were economy-wide. Among those targeting specific sectors, the most supported were manufacturing, energy and agri-food.

Brazil followed with only 264 programmes. Of this total, 253 were loans and 227 targeted specific sector. What distinguishes Brazil is its clear strategy: support specific economic activities (mainly agri-food and industry) with direct credit. For example, the government’s annual Agricultural and Livestock (SAFRA) Plans, budgeted at USD 9.6 billion for its latest edition, offer a series of loans year-round. The country’s latest industrial policy plan initially allocated USD 36.5 billion in loans.

Russia is the only country where guarantee programmes outnumber loans. Out of the country’s 104 recorded programmes, 56 were guarantee schemes. They were also skewed toward metals and derivative products, defence, and transport goods. For example, the USD 2.2 billion guarantee scheme for “technological sovereignty” sectors spans aviation, automotive, railway and other industries, and the USD 367.3 million allocation to the Project Finance Factory programme targeted pre-identified “priority” sectors, including manufacturing and metallurgy.

The Rise of National Financial Institutions

One thread runs consistently across most jurisdictions: the rise of national financial institutions (NFIs) as a preferred delivery channel. NFI-implemented schemes jumped from 33 in 2019 (a record at the time) to 148 in 2020, and they averaged 119 between 2021 and 2025.

Brazil, the Republic of Korea and the EU rely heavily on NFIs. In Brazil, 72% of programmes are channelled via NFIs, with BNDES, the national development bank, as the primary vehicle. In fact, both the SAFRA and industrial loans highlighted in the previous section are mainly delivered by BNDES. In Korea, over 52% of support is channelled via NFIs across a cluster of national banks. These include the Korea Development Bank (KDB), the Industrial Bank of Korea (IBK), the Export-Import Bank of Korea (KEXIM), the Korea Credit Guarantee Fund (KODIT) and the Korea Technology Finance Corporation (KOTEC). This is most clearly illustrated by the 2024 pledge to jointly mobilise USD 313.8 billion in new financing until 2030. Germany, France, Italy, and Spain all channel programmes through dedicated development banks or export credit agencies. In 2025 alone, Germany launched a USD 35.2 billion Germany Fund coordinated by KfW, and Spain channelled over USD 5 billion in guarantees via its Official Credit Institute.

China, however, stands apart. 49% of its programmes are implemented at the subnational level. This reflects a decentralised model in which central policy direction is executed through local authorities. Of the identified state credit programmes, 75% are sector-specific. Manufacturing accounts for 47%, with a recent push for robotics. Agriculture accounts for 31%, channelled through multibillion-dollar agricultural industry development funds.

The Permanent Shifts

The post-pandemic expansion of these instruments shows that governments now treat credit provision as a standing function. They peaked as emergency instruments, but now they are permanent policy features.

Two tensions define this landscape. First, governments have expanded economy-wide lending since the pandemic, although this broadening is not unconditional. Second, the targeted sectors and institutional variation suggest that state capitalism does not follow a single global model. Countries are experimenting with different delivery mechanisms and prioritised sectors. Given that loans and guarantees are the principal tools through which modern governments shape economic outcomes, these shifts deserve close scrutiny.