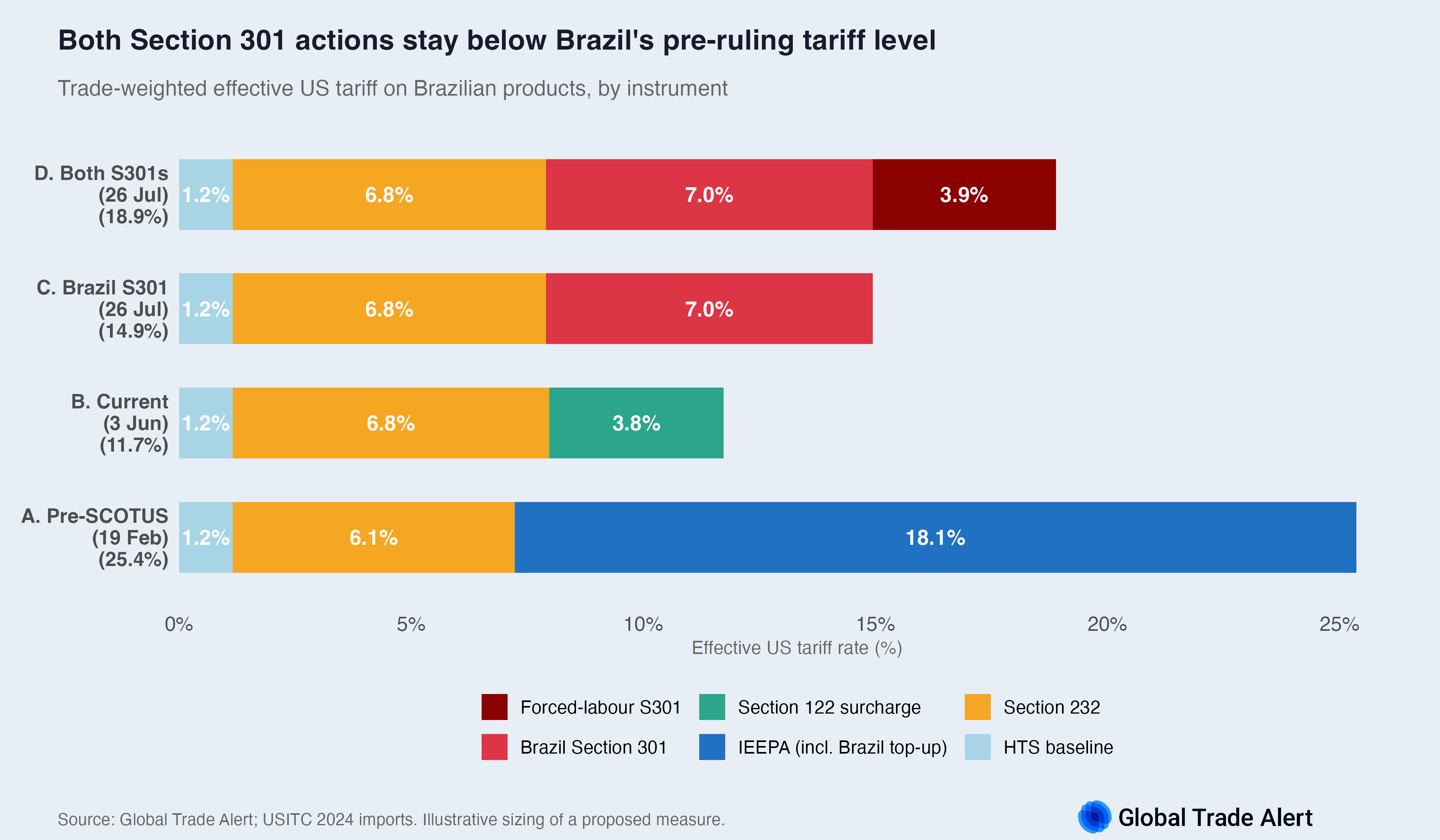

Both Section 301 actions would leave Brazil below its pre-ruling tariff level

On 1 June 2026 the Office of the US Trade Representative proposed a 25% Section 301 tariff on Brazil imports. The action is a proposal: comments close on 1 July, a hearing is set for 6 July, and no effective date is named.

We analyse how US import tariffs level would change from today under two scenarios. First, the implemention of this Section 301 as currently propsed. Second, we add to this burden the implied tariff levels for the Section 301 determination on forced-labour, which also includes Brazil. Both scenarios assume that the current Section 122 tariffs lapse before the Section 301s go into effect.

Both scenarios sit below the 25.4% Brazil faced before the SCOTUS ruling. For context: if the Section 122 surcharge expired on 24 July with no Section 301, Brazil would sit at 7.9%.

The Section 301's would shift Brazil's market access sharply, but the tariff level remains below its February level. Before the SCOTUS ruling, IEEPA imposed a 10% baseline plus a 40% country surcharge on most goods, for a trade-weighted 25.4%. The strike-down removed the IEEPA layer entirely. The Section 122 surcharge provides a temporary replacement, bringing Brazil to 11.7% today. Without new action, Brazil would settle at 7.9% on ordinary tariffs and Section 232 alone. The proposed Section 301 is the durable instrument that would apply a Brazil-specific duty once the emergency measures lapse. It recovers part of the pre-ruling burden, but the carve-outs keep it below the pre-ruling level.

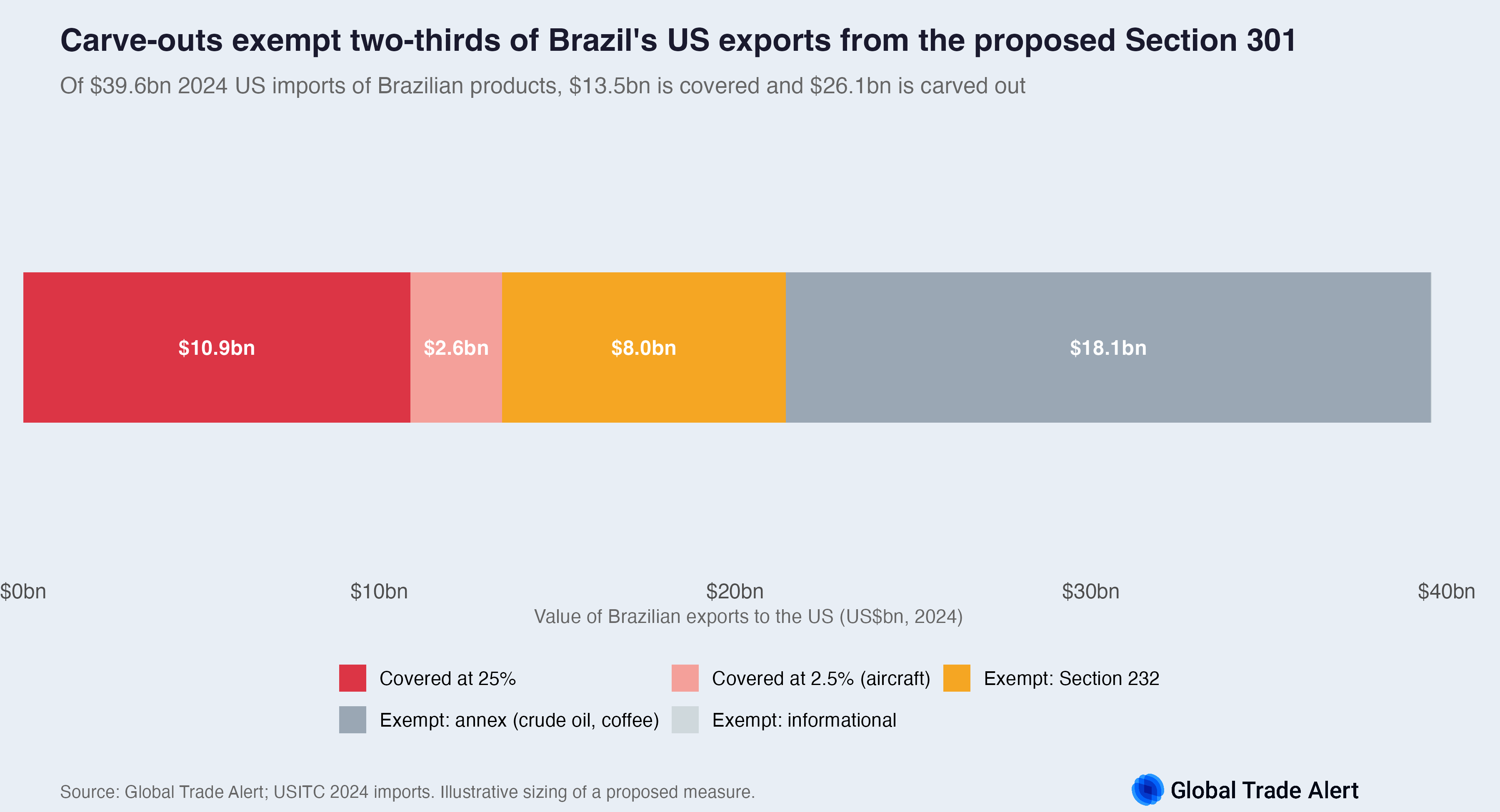

A blanket 25% covers only a third of Brazil's exports

Like IEEPA, the Brazilian Section 301 is formulated as a negative list: 25% on everything, then exclusions. The scope is defined by what is excluded. Of $39.6bn in 2024 US imports of Brazilian products, the proposed tariff covers $13.5bn and excludes $26.1bn. The annex exclusions account for $18.1bn, dominated by crude oil and coffee. A further $8.0bn is exempt because Section 232 already applies. This is why a 25% headline rate produces an effective rate near 15%, not 25%.

The aircraft assumption understates the likely exposure

One carve-out warrants attention because it affects the bounds of our estimate. The annex designates 546 subheadings worth $2.6bn as "Aircraft", excluding only civil-aircraft articles within them. Since the Section 301 layer is not otherwise weighted by civil-aircraft share, we apply that assumption to the rate: assuming 90% of the trade on those lines qualifies as civil, we model an effective 2.5% rather than the full 25%. This assumption understates the duty to the extent the true civil share is lower. If none of that trade qualified as civil, the Section 301 duty would rise from $2.8bn to roughly $3.4bn, and Brazil's effective rate from 14.9% to approximately 16.4%. The actual figure lies between these bounds, closer to our estimate the larger the genuine civil-aircraft share.

This assumption is testable. The full model is available as a Global Trade Alert tariff MCP server. The civil-aircraft share, in-force date, and headline rate are all adjustable parameters. Use the GTA MCP to can change them, re-run the estimate, and observe how the covered trade and effective rate change.

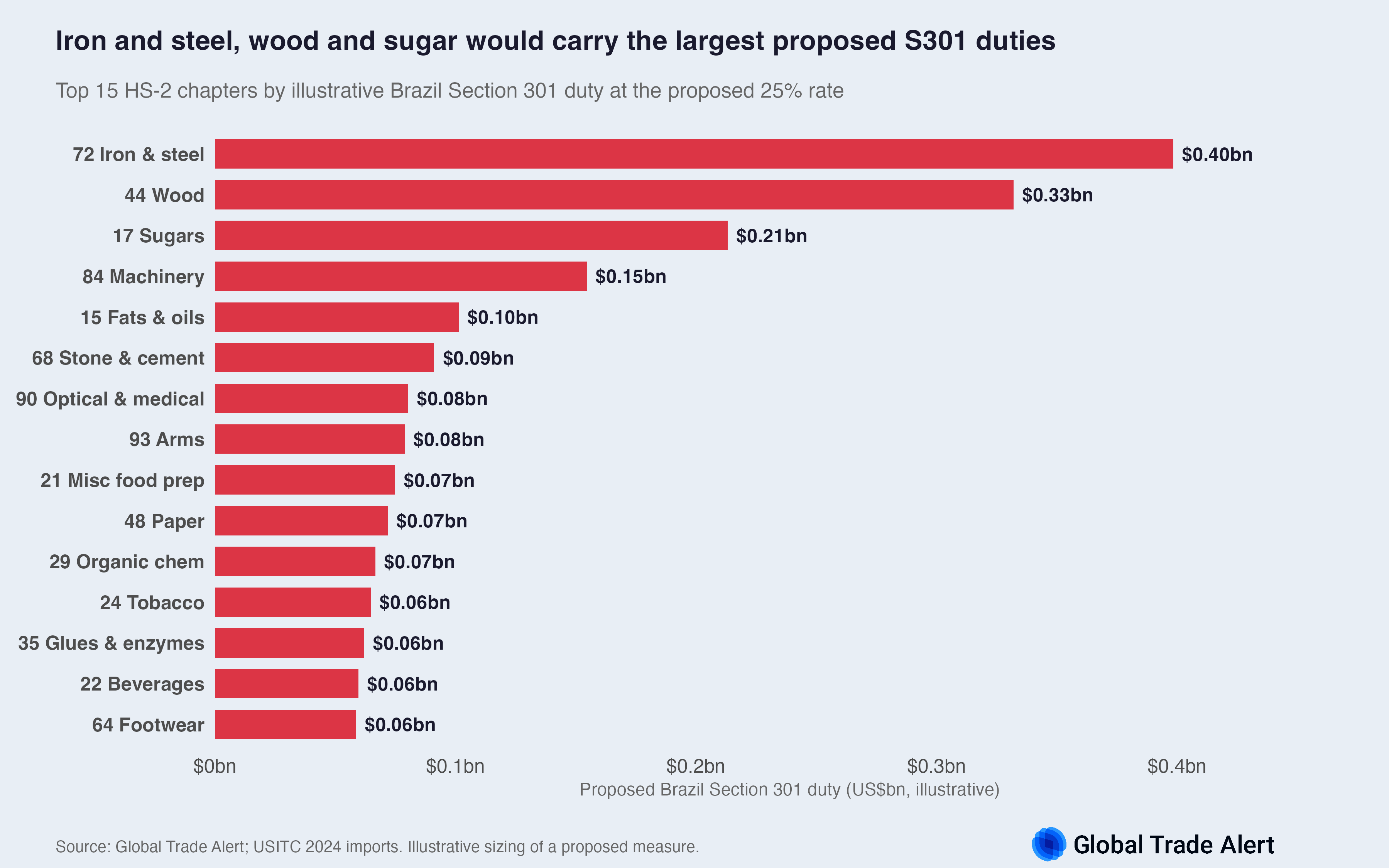

The duty lands outside the Section 232 scope

Because Section 232 goods are excluded from the Section 301, the new duty concentrates where Section 232 does not apply. The single largest exposed line is not finished steel, which is already covered, but pig iron (HTSUS 7201), a raw input outside the Section 232 steel scope. That one line carries $1.5bn of the covered trade. Wood follows, but the exposed portion is plywood and joinery rather than the softwood lumber that Section 232 covers. Sugar has no Section 232 shelter at all. The pattern is consistent across the exposed goods: the 25% applies hardest to Brazilian products that earlier tariff instruments left untouched.

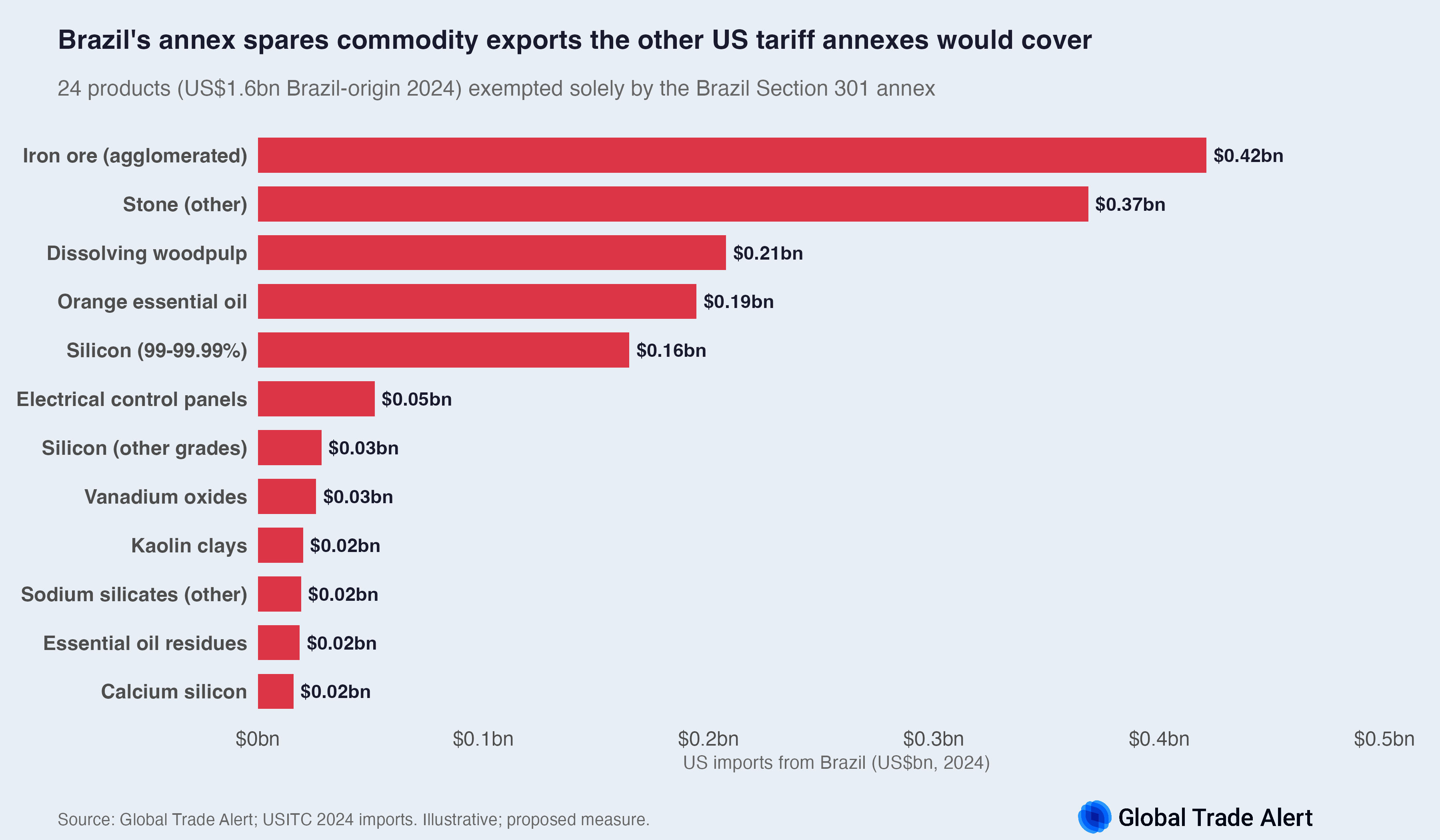

Products exempted by the Brazil annex alone

There are just over 40 products exempted solely by the Brazil annex: the forced-labour Section 301 and Section 122 annexes do not carry equivalent carve-outs. Of these, 24 carry recorded Brazil-origin trade, amounting to $1.6bn of 2024 US imports. The leading items are agglomerated iron ore ($0.42bn), stone ($0.37bn), dissolving woodpulp ($0.21bn), orange essential oil ($0.19bn), and silicon ($0.16bn).

Status and method

Both Section 301 actions are proposals, not in force. The figures here are illustrative scaling on 2024 trade weights, not a forecast; they assume an in-force date of 26 July 2026, after the Section 122 surcharge lapses and with IEEPA already struck. They exclude HTSUS Chapter 98 (US goods returned and similar special provisions). The underlying data are available below, and the model itself can be queried and re-parameterised through the Global Trade Alert tariff MCP.

Downloads