Trade securitisation is moving from goods to services. Governments enacted 327 security-justified measures affecting services in the first half of 2026, more than in any full year before 2025. Global Trade Alert data shows that most are Western sanctions, but the shift survives their removal. The evidence also shows that the supply chain resilience measures reaching services concentrate in cloud and AI infrastructure.

Authors

Ana Elena Sancho

Date Published

15 Jul 2026

Related Topics:

Governments are securitising services trade at a rising volume. In the first half of 2026, they enacted 327 security-justified measures affecting services, more than in any full year before 2025.[1] This piece traces where trade securitisation is spreading across services and where it concentrates, drawing on all security-motivated measures recorded in the Global Trade Alert (GTA) since 2022. The relevant measures include sanctions and countersanctions. Both enter the count on the same basis as every other measure: they carry an explicit security rationale in the GTA record. We report our findings with and without them, so the reader can see what sanctions add.

Security-motivated activity is shifting from goods toward services

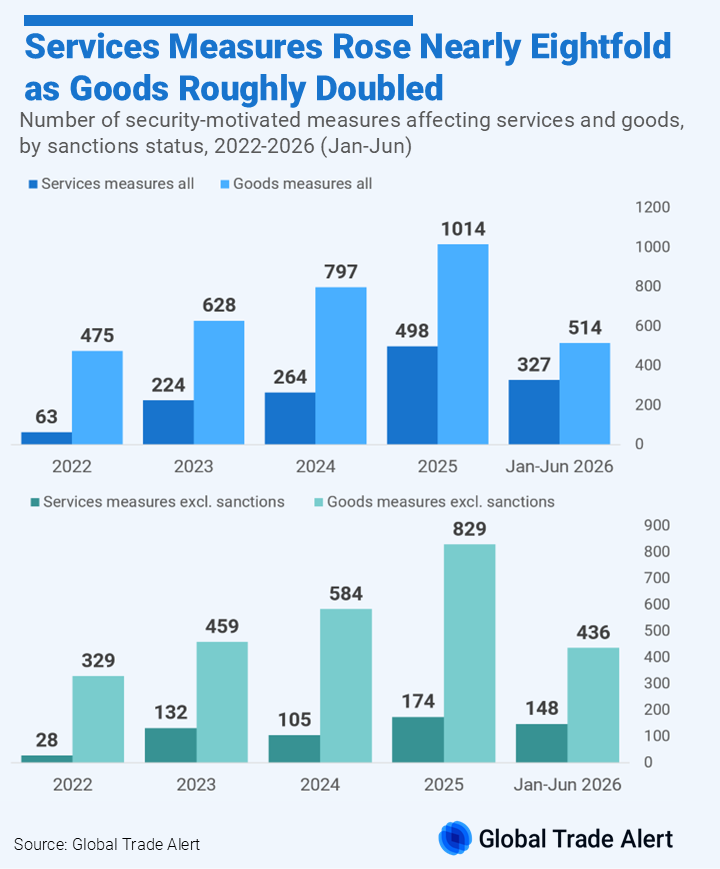

Security-motivated trade activity is moving from goods toward services (see Figure 1). Services rose from 12% of the security-justified universe in 2022 to 42% in 2026. Goods fell from 94% to 66% over the same period.[2] This does not mean governments have reduced their securitisation of goods in absolute terms. Securitisation activity of goods roughly doubled between 2022 and 2025. However, security-justified measures affecting services rose nearly eightfold over the same years.

The movement toward services is not explained by sanctions alone. Western sanctions tied to the conflicts involving Russia and Iran account for the largest share, spanning financial services and shipping insurance. Arguably, because they target specific geopolitical concerns, they may reflect those conflicts rather than a broad turn toward securitising services. Excluding sanctions-linked measures, services measures still rose more than sixfold between 2022 and 2025, against roughly two and a half times for goods. Sanctions therefore amplify the shift but do not explain it.

Western sanctions stand for the geopolitical motivation for services securitisation

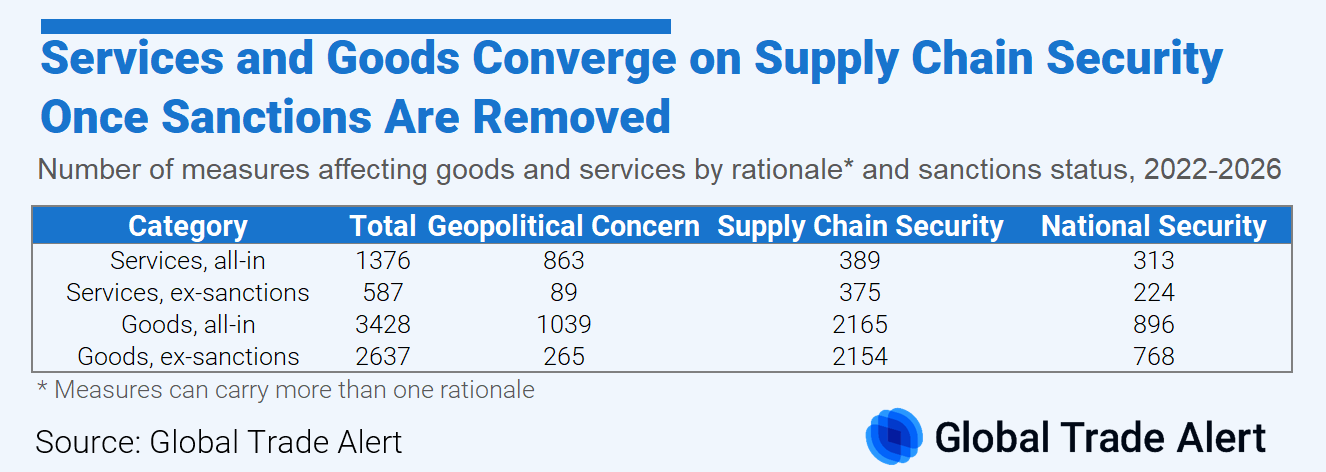

Sanctions account for 57% of security-justified services measures since 2022 (see Figure 2). The main implementers are the United States, the European Union, the United Kingdom, Canada, Switzerland, and Australia. Together, these jurisdictions account for 79% of sanctions-linked services measures. These measures include asset freezes like the April 2026 US Treasury sanctions on financial services, as well as service provisions controls like the UK’s May 2026 prohibition on participating in the maritime transportation of Russian liquefied natural gas, among others.

Set the sanctions aside, and services securitisation rests on the same rationale as goods. As Figure 2 shows, across 2022 to 2026, governments cited geopolitical concern for services measures just over twice as often as supply chain security motivations. Excluding sanctions-linked measures, that ratio falls well below one to one. Supply chain security then becomes the more common rationale for services, as it already is for goods.

Securitised services activity concentrates in six categories, and its supply-chain core sits in technology

Within services, security-justified activity concentrates in six categories (see Figure 3). Maritime support, cloud and IT, financial services, aerospace and satellite, telecommunications, and insurance services account for 59% of the services-affecting measures since 2022. Maritime support and cloud and IT are the largest categories, at 24% and 23%. Excluding sanctions-linked measures, that share falls to 44%, so the concentration is substantially sanctions-driven.

Where securitisation of services rests on supply chain security alone, it concentrates in one sector group. Of 86 services measures citing supply chain security without any geopolitical or national security rationale, 59 fall under management consulting and information technology services. None of these measures is sanctions-linked. The IT measures in this group mainly refer to cloud, data centres, and AI schemes. For example, in May 2026, Thailand's Board of Investment granted tax incentives for two large data centre projects: one located in Chachoengsao and the other in Chonburi. Similarly, in June 2026, the European Commission proposed a Cloud and AI Development Act that would restrict public-sector cloud procurement to EU-established providers to reduce reliance on foreign providers.

The resilience logic is reaching frontier services

The securitisation of trade is extending to services, and the shift holds whether or not sanctions are counted. Setting sanctions aside, it is a supply-chain story rather than a geopolitical one, and it concentrates on IT services. The resilience logic that has long organised the securitisation of goods, building capacity and reducing dependency, is now reaching the services that sit at the technological frontier.

1

By security-motivated measures, this piece means policy interventions that include any one of the following stated motives as codified in the GTA database: “national security”, “supply chain security” and “geopolitical concern”.

2

The two shares overlap because a measure can affect both, and they do not sum to the universe.