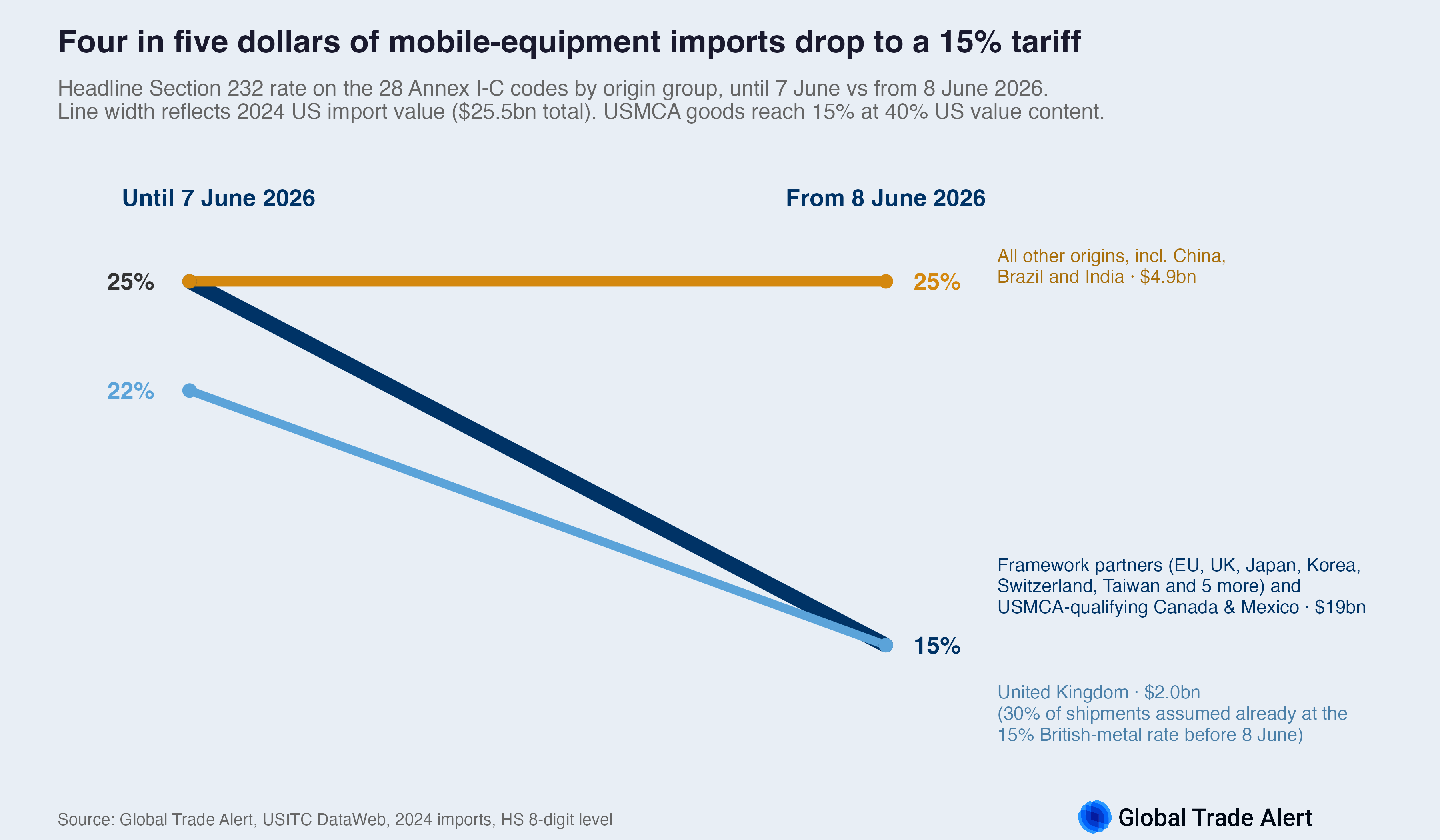

Section 232 rates on mobile equipment now depend on origin

A proclamation of 1 June 2026, in force since 8 June, modifies the Section 232 metals regime. The largest change is a new product annex, I-C, whose tariff depends on origin. Until 7 June, suppliers of forklifts, earth-moving machinery, non-agricultural tractors and mobile cranes paid 25%, with partial relief only for goods made of British metal. From 8 June, the European Union, the United Kingdom, Japan, Korea, Switzerland, Taiwan and five other partners pay 15%, USMCA-qualifying Canadian and Mexican goods pay close to 15%, and others continue at 25%. A preference that applied only to the United Kingdom now covers 37 economies.

Four in five dollars of these imports see their tariffs reduced to 15%, led by Japan at $6.9 billion in 2024. China, Brazil and India remain at 25%. The United Kingdom starts at around 22%, an average of the 15% its British-metal shipments paid under the 2025 agreement and the 25% on the rest. From 8 June the 15% no longer depends on metal content and covers every framework partner.

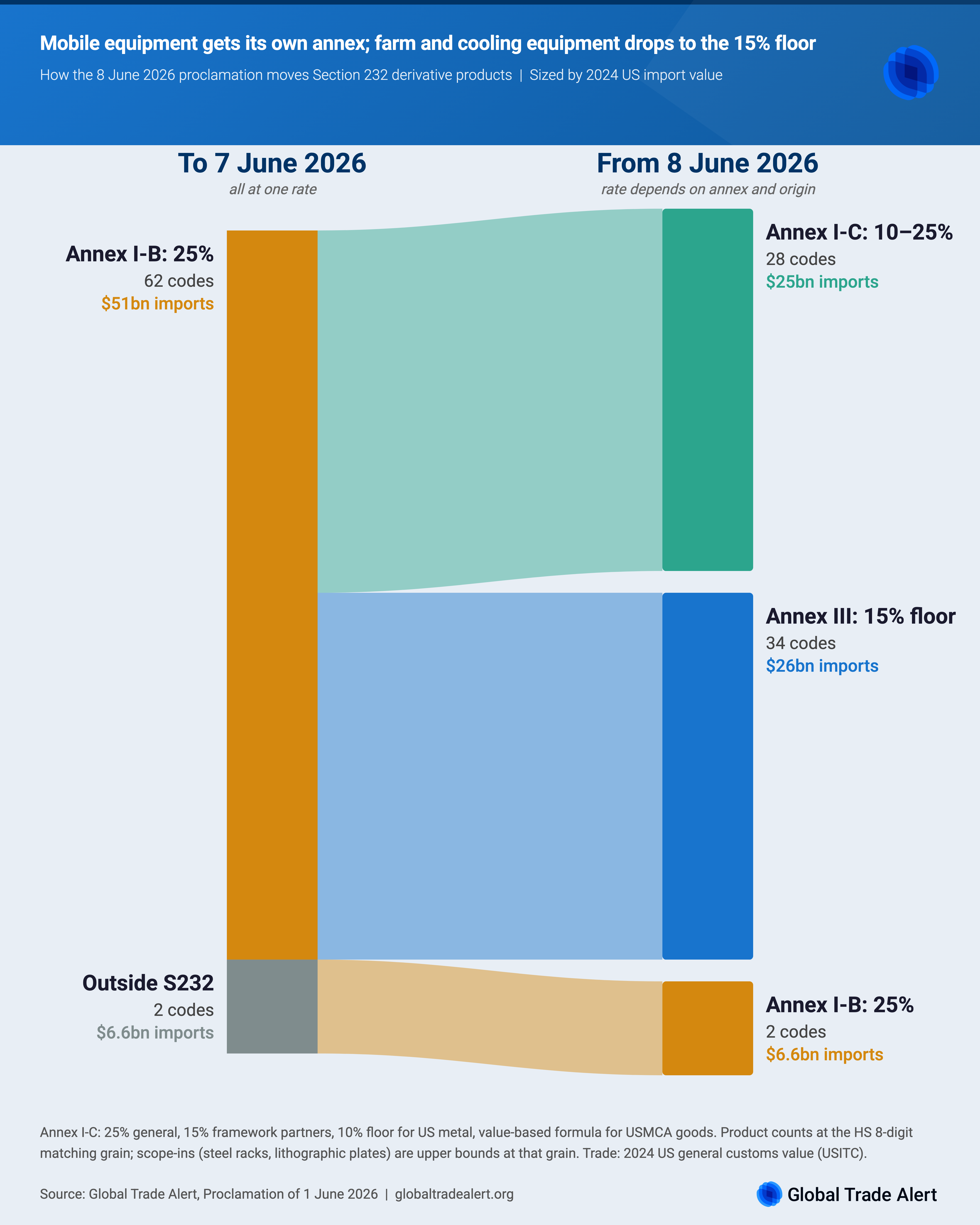

The other changes point the same way: 39 product codes for agricultural equipment and residential air-conditioning move to a 15% floor across all origins, and aluminium lithographic plates and steel racks enter Section 232 at 25%. Annual duty falls by $3.4 billion across the roughly $58 billion of affected imports. The trade-weighted average US tariff moves from 10.8% to 10.7%.

Where the products went

The Annex I-C and Annex III moves are temporary, expiring 31 December 2027, after which products revert to 25%. The scope additions are permanent, as is the reduction of the US-metal threshold for the 10% rate from 95% to 85% by weight. Steel racks now pay 25% under Section 232 instead of 10% under Section 122, raising duties by $0.9 billion annually. The other moves reduce duties by $4.3 billion.

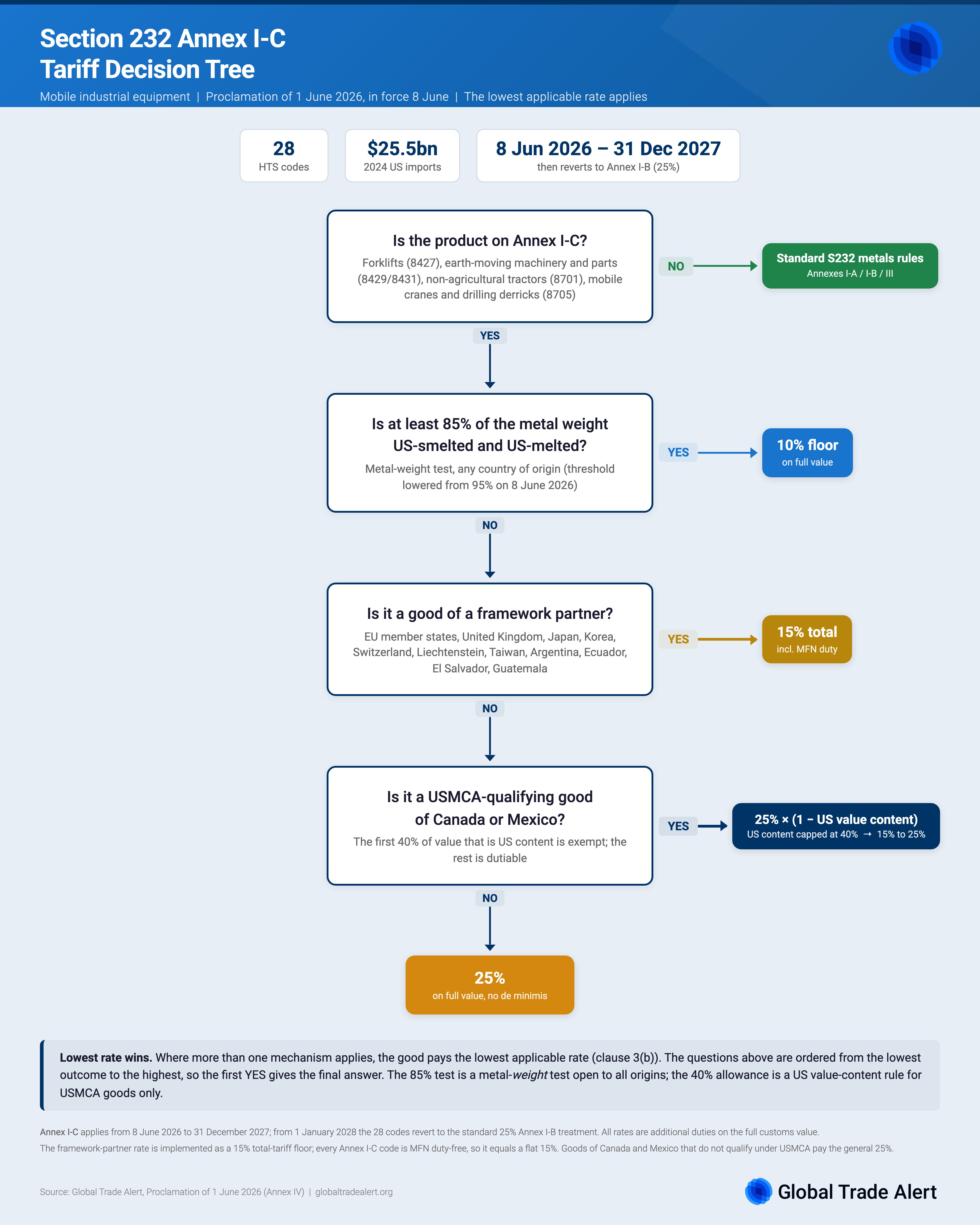

How the Annex I-C rate is determined

Three preferential mechanisms overlie the same 28 codes, and the lowest applicable rate wins. They test different things, on different bases, for different countries:

Note that two thresholds test different things: the 85% is a metal-weight test open to any origin, the 40% is a value-content allowance for Canada and Mexico only. A USMCA-qualifying Canadian forklift with 60% US content pays 15% because the exemption applies to at most 40% of value; the duty falls on the rest. A decision tree below walks through the full logic.

Status and method

The proclamation is in force. Estimates compare the same tariff model at two policy dates (7 and 8 June 2026) against 2024 US import values and the 2024 HTS schedule. Product matching runs at the HS 8-digit level; the newly scoped types are 10-digit lines, so their $6.6 billion figure is an upper bound. Not modelled: the routing of parts into reduced-rate headings, and one steel-rack code whose heading overlaps a civil-aircraft exemption.

Downloads