What is changing, and what is not

On 2 June 2026 the Office of the US Trade Representative proposed Section 301 tariffs on substantially all goods of sixty economies it had investigated for failing to prohibit or enforce against imports made with forced labour. It is a proposal: comments close on 6 July, a hearing is set for 7 July, and the notice sets no effective date. The duty has two rates, 10% for fourteen economies and 12.5% for the other forty-six. It is structured as a negative list, applying to all goods of each economy in scope except those on a shared annex.

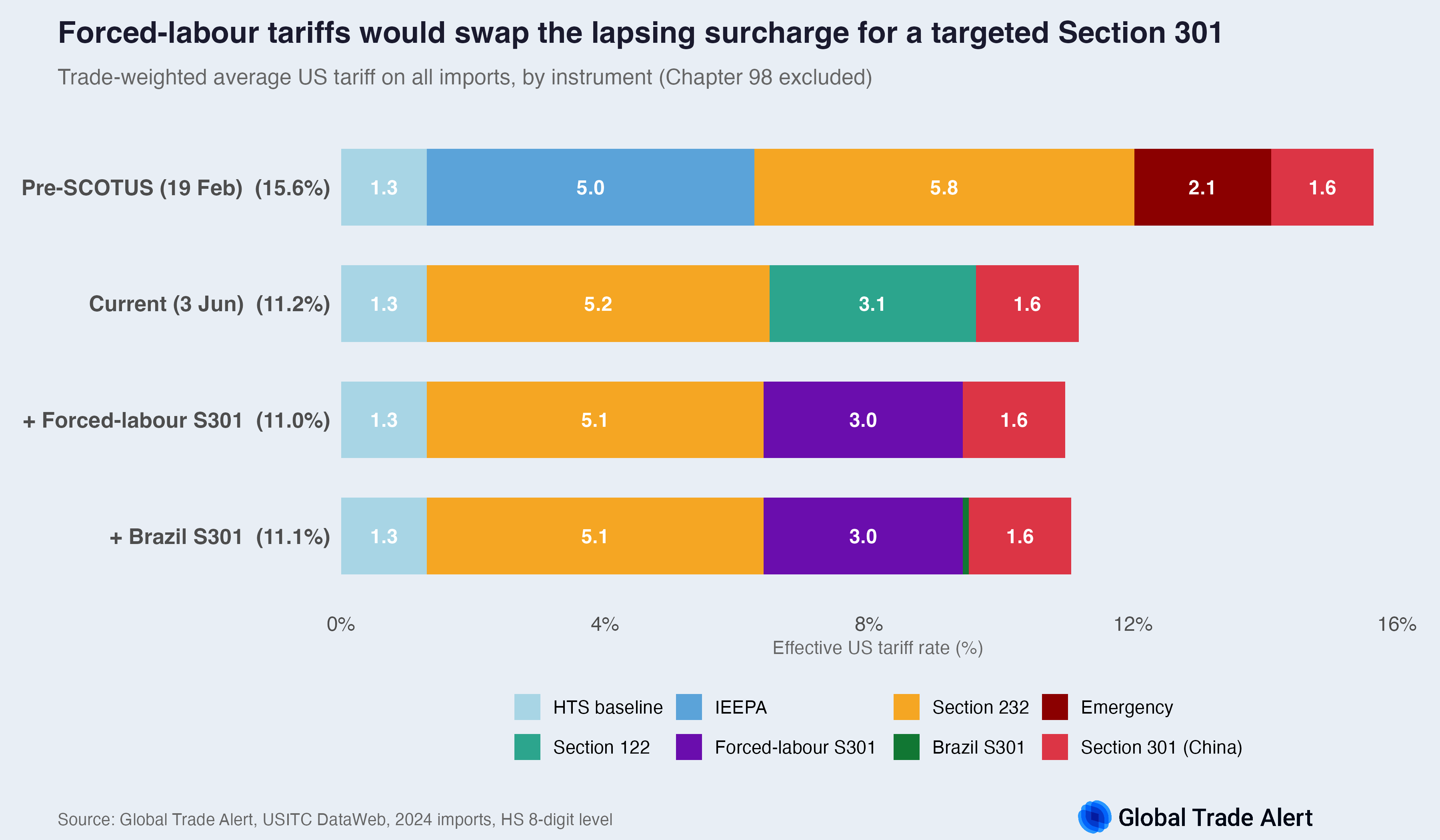

The main finding is what does not change. In effect the proposal exchanges a broad surcharge on almost all imports for a targeted duty on sixty economies, holding the overall level roughly steady rather than raising it. As the temporary Section 122 surcharge lapses on 24 July, the forced-labour Section 301 would step into its place and leave the US average effective tariff close to where it is today. On 2024 import values the trade-weighted average is 11.2% under the current regime and 11.0% with the forced-labour duty in force; adding a separately proposed Brazil Section 301 brings it to 11.1%. The Section 232 duties on metals, vehicles and related goods remain the largest single component throughout.

To show this, we read the GTA's US tariff model at four states of the regime, on 2024 import values. Each state is the model read at a different date; the two proposed Section 301 actions are dated to an assumed 26 July 2026, after the Section 122 surcharge has expired.

- Before the Supreme Court ruling (19 February 2026): MFN duties, the IEEPA tariffs, and Section 232 duties. The trade-weighted average US tariff is 15.6%.

- Current regime (3 June 2026): MFN duties, the Section 122 surcharge, and Section 232 duties; the IEEPA tariffs have been struck down. The average is 11.2%.

- With the forced-labour Section 301 (assumed in force 26 July 2026): MFN duties, Section 232 duties, and the forced-labour Section 301; the Section 122 surcharge has expired. The average is 11.0%.

- With the forced-labour and Brazil Section 301s (assumed in force 26 July 2026): the same, with the separately proposed Brazil Section 301 added. The average is 11.1%.

The average moves little because the proposed duty, broad on paper, is closely bounded in practice and overlaps with tariffs already in force. The chart shows the composition of the average tariff at each state. The sections below trace where the duty applies, where it does not, and how the average rate shifts between economies.

What the new Section 301s cover

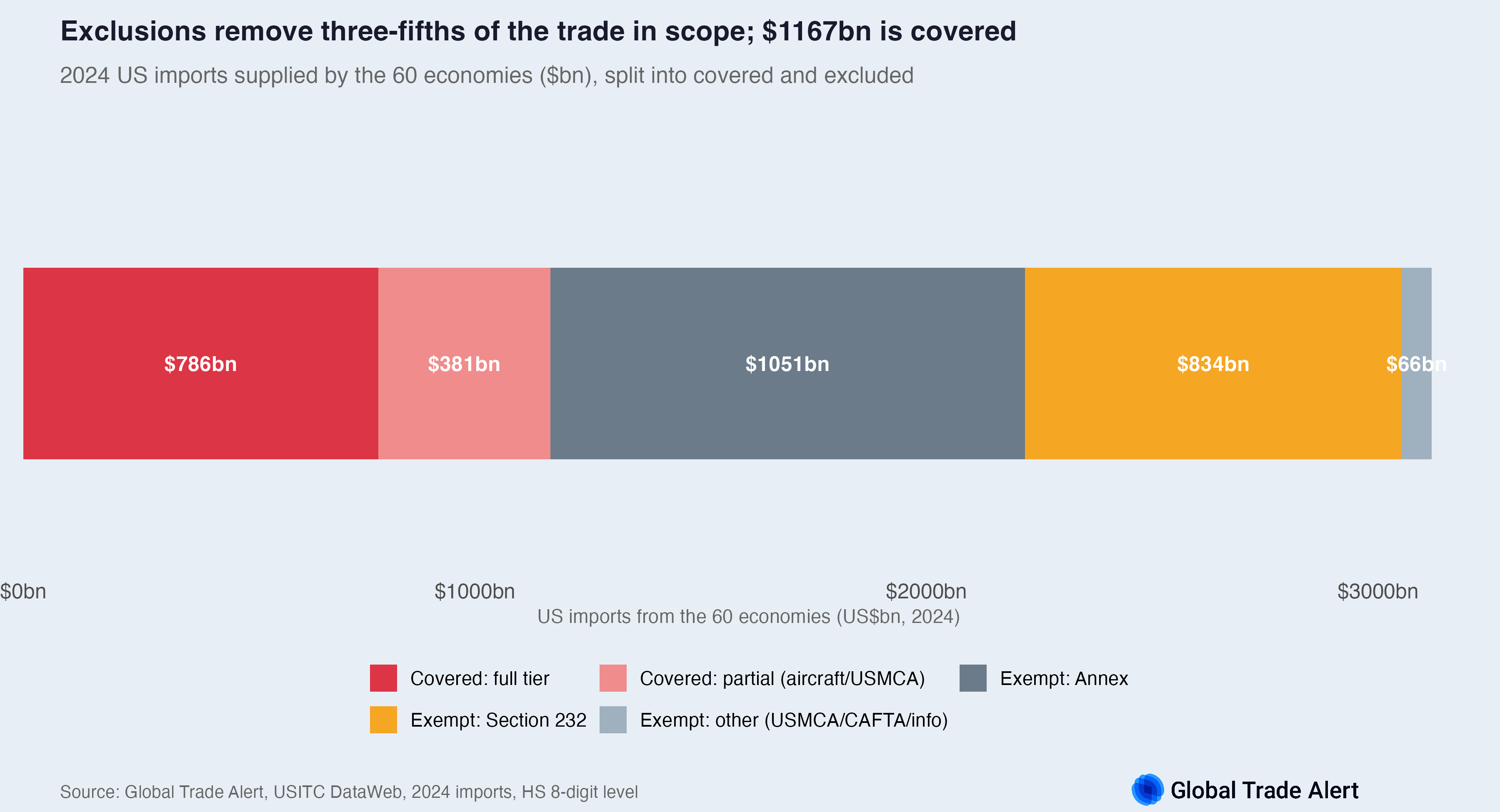

The reason the average barely moves is in the scope. Reading it means reading the exclusions. Of the $3,119 billion supplied by the sixty economies, the exclusions remove about three in five dollars, leaving about $1,167 billion the duty would cover. Two exclusions do most of the work: the shared annex, and the rule that goods already subject to Section 232 duties are excluded. USMCA-compliant goods of Canada and Mexico, the civil-aircraft share of aircraft lines, CAFTA-DR textiles and informational materials account for the rest. Much of what the new duty would otherwise reach is already carried by Section 232, so layering the Section 301 on top adds little to the average.

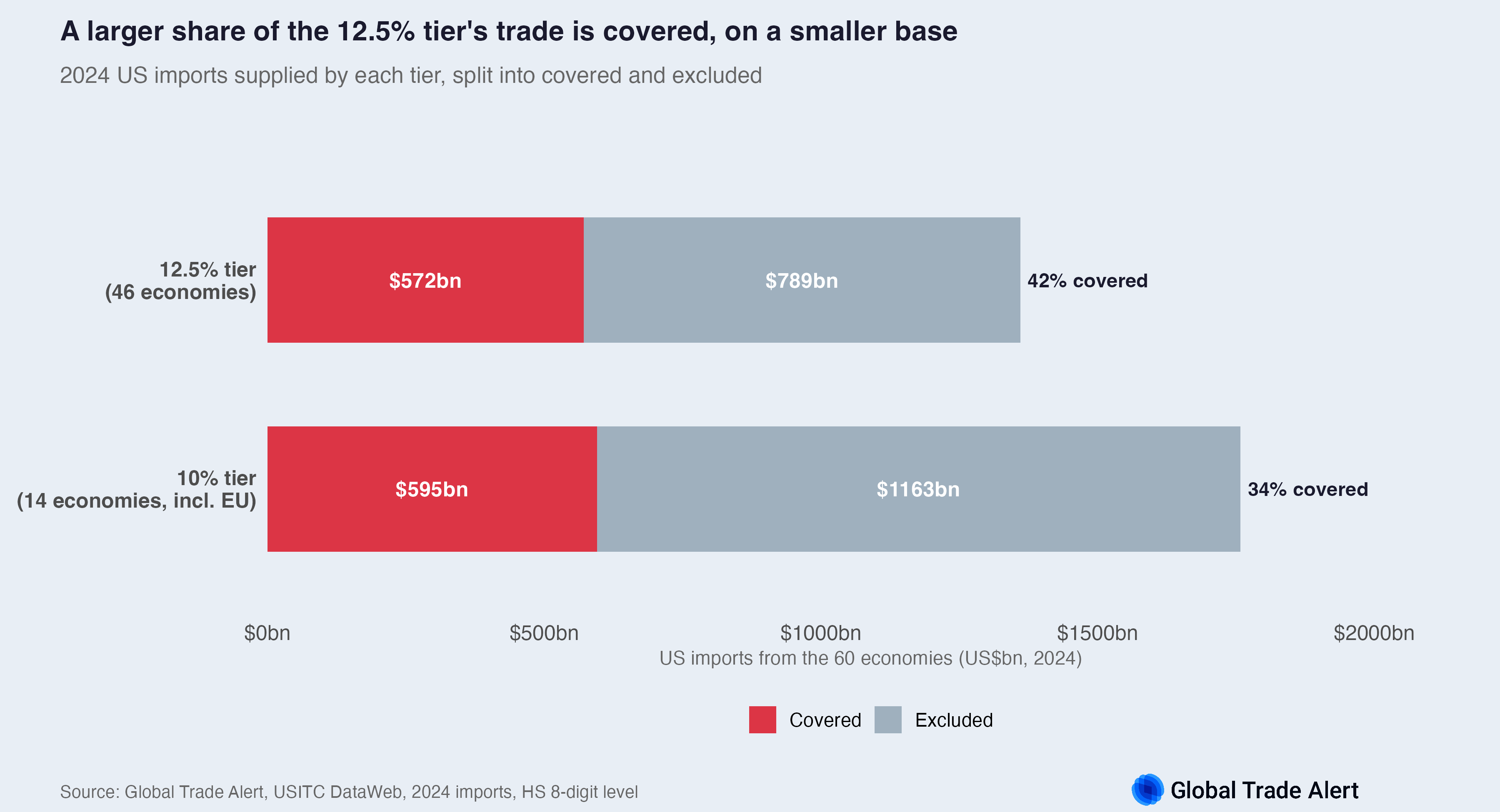

The two tiers

The 10% tier covers fourteen economies, including the European Union counted through its member states. They supply about $1,758 billion of US imports, of which the duty would cover about $595 billion, roughly a third. The 12.5% tier covers forty-six economies, including China, Japan, India and Brazil. They supply less, about $1,361 billion, but a larger share is covered, about $572 billion or two in five dollars, because the annex and the Section 232 exclusions remove less of their trade.

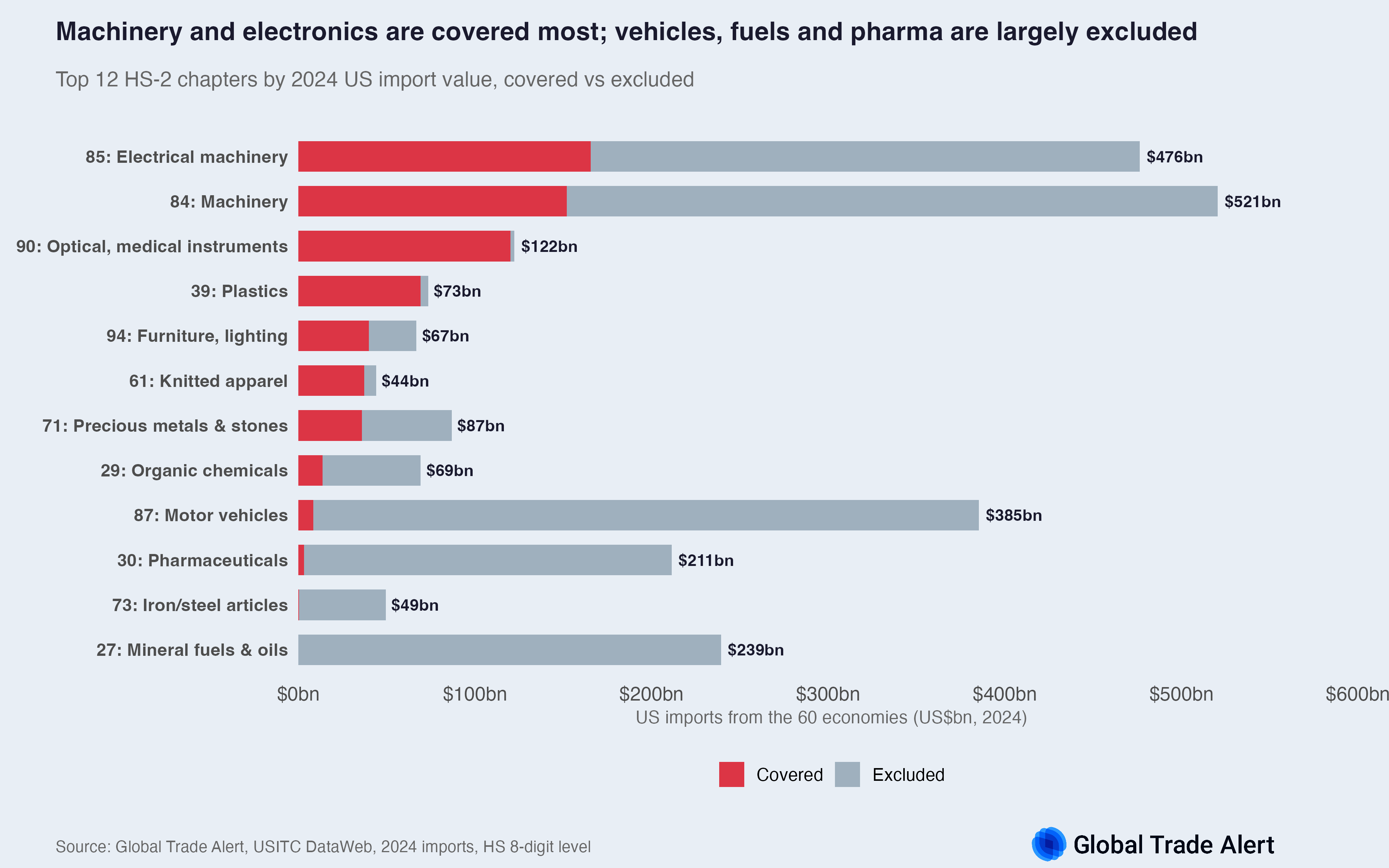

Which sectors are covered

Machinery and electrical equipment account for most of the covered trade, as large import categories that the Section 232 actions on metals and vehicles do not cover. Motor vehicles, mineral fuels and pharmaceuticals are mostly outside the duty, the first two through Section 232 and the annex, the third through the annex. Optical and medical instruments, plastics and apparel are covered in large part.

How the burden shifts between economies

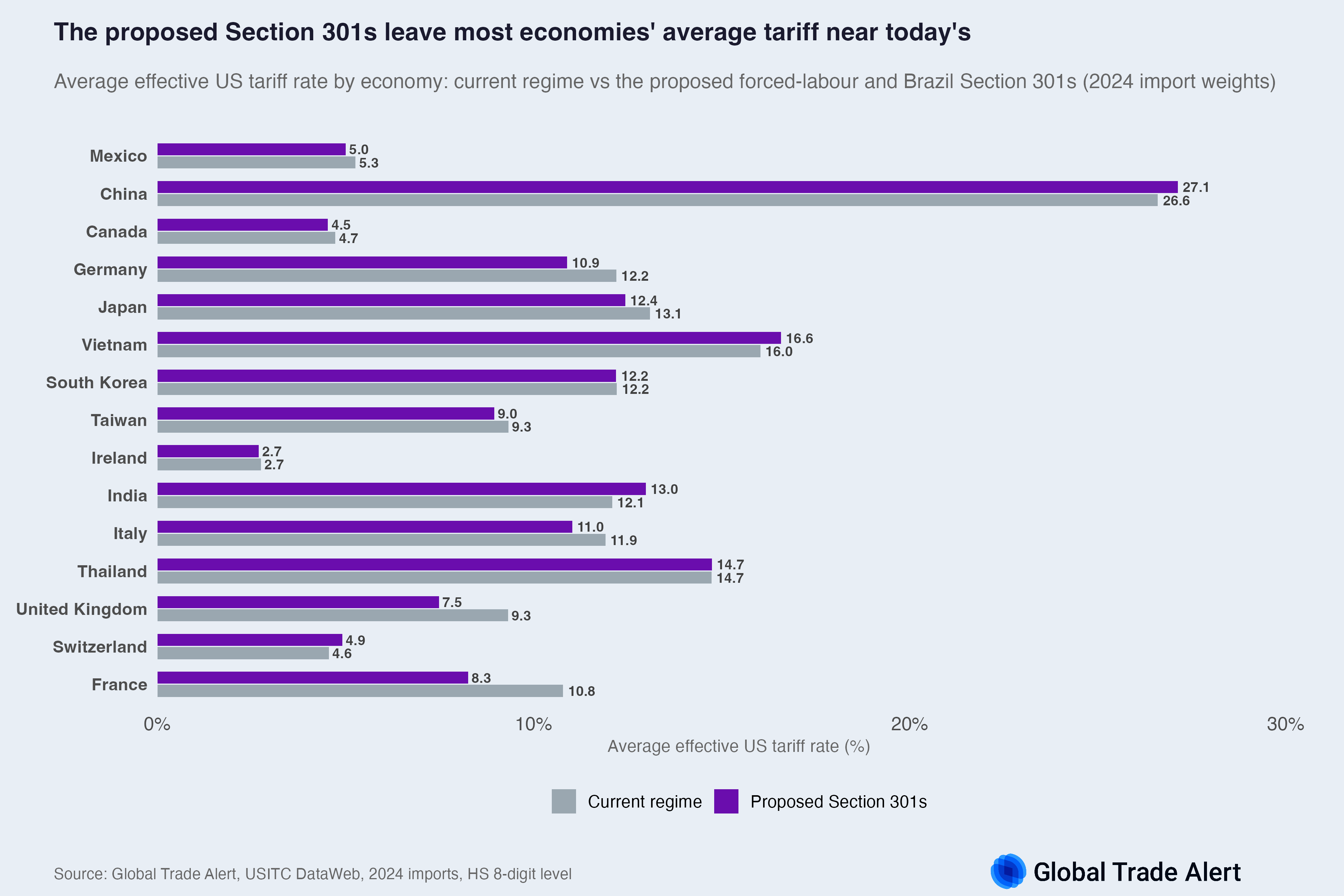

Because the Section 301s reach sixty economies rather than all imports, they redistribute the tariff burden even as they hold the average steady. The chart below gives the average effective US tariff each economy faces under the current regime and under the proposed Section 301s. For most large suppliers the rate barely moves. China, already the most heavily tariffed through its existing Section 301 and the Section 232 duties, stays near 27%. Mexico and Canada remain close to 5%, because both hold a USMCA exemption that covers much of their trade.

The visible shifts are modest and follow the tier split. Economies in the 10% tier, including the European Union's larger members, see their average ease a little as the broad Section 122 surcharge lapses and the targeted duty covers only part of their trade: Germany moves from 12.2% to 10.9%, France from 10.8% to 8.3%. Economies in the 12.5% tier, such as Vietnam and India, edge up by roughly half a point to a point. The aggregate changes little because the economies left outside the sixty add little to US imports, so leaving them out costs little at the average, while the sixty in scope exchange one broad instrument for a targeted one.

A fall may surprise where the rates look identical: the surcharge and the 10% tier carry the same headline rate, so for the European economies the change comes from the base, not the rate. The Section 301 grants exclusions the surcharge did not, and the aircraft treatment matters most. Aircraft and jet-engine lines paid the surcharge in full, but under the proposed duty only their estimated non-civil share, a tenth of their value, is dutiable, an effective rate of about 1% rather than 10%. That is why France, whose US-bound exports are heavy in airframes and jet-engine parts, falls furthest among the large European suppliers; the annex exclusions, which remove much of its machinery trade, account for most of the rest of the gap.

Downloads

The following dataset is available for download:

- Forced-labour Section 301 dataset: the average effective tariff rate by economy under the current and proposed regimes, the covered and excluded import values, the tier and sector breakdowns, the exclusion decomposition, and the flow-level table at the exporter and HS 8-digit level for all four states.