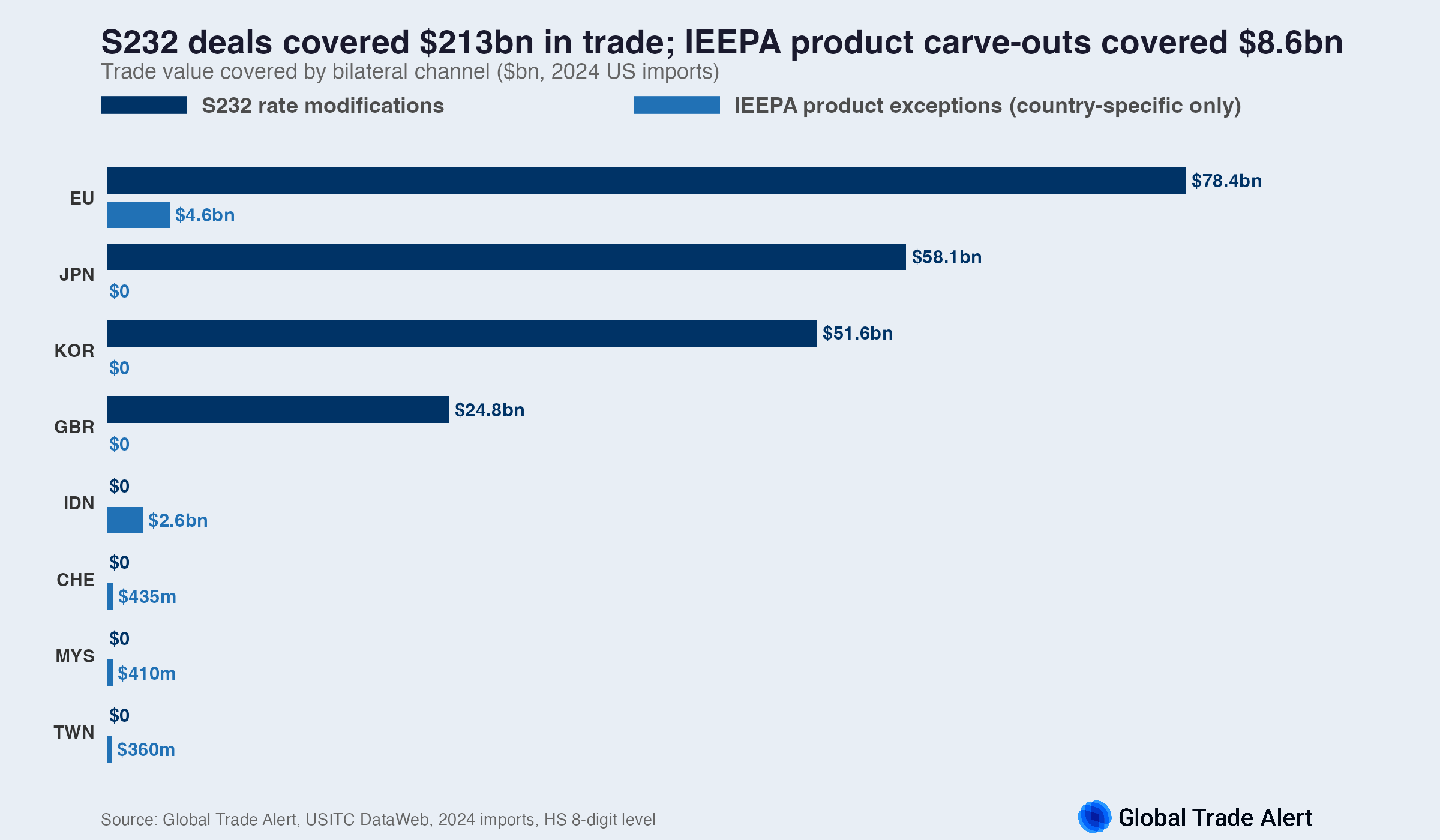

Trading partners should not mistake the Supreme Court's February 20 ruling for commercial relief. The bilateral tariff concessions that mattered most were never built on IEEPA. They were built on Section 232, the national security statute under which the administration has imposed tariffs on products from steel to semiconductors, and on Section 301, the statute that authorises retaliation against unfair foreign trade practices. Negotiated rate reductions under Section 232 alone covered $213 billion in trade across four countries, roughly 25 times the $8.6 billion in product carve-outs negotiated under IEEPA.* Both statutes remain untouched by the ruling, and this time the Supreme Court may not be coming to the rescue. Furthermore, it is true that these statutes require investigation processes that IEEPA did not. But observers who expect that procedural difference to buy time should take note how fast the administration compressed a Section 301 process last November.

Section 232 rate reductions dwarfed IEEPA product carve-outs

Section 232 rate modifications dominated the bilateral negotiations for the largest deal partners. The United Kingdom, Japan, and South Korea skipped IEEPA product exception lists entirely, focusing instead on rate reductions for steel, aluminium, and automobiles. The EU pursued both channels, but its Section 232 arrangements covered far more trade than its IEEPA product exceptions.

The EU's deal was the largest: The trade volume within its Section 232 automobile deal alone ($76.5 billion) dwarfed its IEEPA product exceptions by 16 to 1 ($4.6 billion). Indonesia was the only country among the fifteen bilateral partners where IEEPA product-level exceptions mattered disproportionately: it had no significant steel, aluminium, or automobile exports to the US and thus no Section 232 exposure.

For every other deal partner, wherever Section 232 rate modifications were available, they dominated the bilateral negotiations.

- Japan's deal covered $58.1 billion, entirely in automobiles and medium/heavy-duty vehicles.

- Korea's deal covered $51.6 billion, entirely in automobiles.

- The United Kingdom's deal covered $24.8 billion, split between automobiles ($12.1 billion) and steel and aluminium ($12.7 billion). The UK was the only country to negotiate differentiated rates across product categories.

Nearly half of Section 232 trade received almost no deal relief

The administration's Section 232 leverage extends well beyond the concessions already granted. Deal rate reductions covered $213 billion, but these four countries' total Section 232 trade is $384 billion. The gap is almost entirely steel and aluminium, for which only the UK secured a rebate. The table below shows each country's full Section 232 exposure. Parenthetical rates indicate the standard rate and, where applicable, the negotiated deal rate.

| Country |

S232 trade |

Auto/MHDV |

Steel |

Aluminium |

Copper |

Lumber |

| EU |

$195bn |

$76.5bn (25% to 15%) |

$97.3bn (50%) |

$16.6bn (50%) |

$1.5bn (50%) |

$2.9bn (25% to 15%) |

| Japan |

$86bn |

$58.1bn (25% to 15%) |

$22.8bn (50%) |

$5.2bn (50%) |

$0.2bn (50%) |

$0.0bn |

| Korea |

$76bn |

$51.9bn (25% to 15%) |

$19.4bn (50%) |

$4.5bn (50%) |

$0.6bn (50%) |

$0.0bn |

| United Kingdom |

$26bn |

$13.2bn (25% to 10%) |

$9.4bn (50% to 25%) |

$3.3bn (50% to 25%) |

$0.1bn (50%) |

$0.1bn (25% to 10%) |

| Total |

$384bn |

$200bn |

$149bn |

$30bn |

$2bn |

$3bn |

Automobiles and medium/heavy-duty vehicles account for $200 billion of the full Section 232 trade from these four countries (52 per cent). Steel and steel derivatives account for $149 billion (39 per cent). Aluminium and aluminium derivatives, net of overlap with steel, account for $30 billion (8 per cent).** Copper accounts for $2 billion (subject to the 50 per cent Section 232 rate with no deal modifications) and lumber for $3 billion (rates of 10 to 25 per cent, with EU and UK derivatives receiving deal reductions to 15 and 10 per cent respectively).

The deals addressed nearly all of the automobile exposure: rate reductions covered 99 per cent of automobile trade within Section 232's scope. Steel and aluminium received almost no deal relief. Only the United Kingdom negotiated any steel or aluminium rate modification ($12.7 billion at a capped rate of 25 per cent, down from 50 per cent). The EU, Japan, and South Korea received no steel or aluminium concessions. Their $166 billion in combined steel and aluminium trade faces the standard Section 232 rate of 50 per cent with no negotiated reduction.

Sections 232 and 301 stand on firmer legal ground than IEEPA

The Supreme Court struck down IEEPA tariffs on a formal question: the word 'regulate' in IEEPA does not encompass setting import duties. That formal gap does not exist in the statutes that will carry the bilateral tariff regime forward. Section 232 of the Trade Expansion Act of 1962 authorises the President to adjust imports of any article that threatens national security, including through tariffs and quantitative restrictions. Section 301 of the Trade Act of 1974 authorises the suspension of trade agreement concessions and the imposition of duties or other import restrictions in response to unfair trade practices. Both statutes explicitly authorise tariffs. (For a side-by-side comparison of the five tariff statutes, see the US Tariff Reference Guide which we published after the election).

Without the formal vulnerability that brought down IEEPA, courts are likely to play a lesser role in checking the administration's tariff actions. Courts have generally deferred on whether the substantive justification behind a trade action is sound. Courts are unlikely to assess whether a trade deficit constitutes an emergency or whether a foreign tax system constitutes a trade barrier. Claussen and Meyer (2024) have documented how the executive branch has used 'economic security' framing to expand its authority over foreign commerce. In their assessment, courts have generally upheld challenged actions even where they stopped short of endorsing the broadest claims of executive discretion.

Investigation timelines may offer less protection than expected

Both Section 232 and Section 301 require investigations before tariffs can be imposed. Section 232 requires a Commerce Department investigation. Section 301 requires a USTR investigation with consultation, public hearings, and a determination; for cases not involving trade agreements, the statute provides 12 months. The fastest precedent, the China investigation of 2017 to 2018, took approximately seven months from initiation to findings and eleven months to first tariff imposition.

That timeline assumes the administration proceeds at a conventional pace. Last November, following the Trump-Xi deal of 1 November 2025, USTR opened a public comment period on a Section 301 maritime and shipbuilding action on 6 November at 12:00 PM EST. It closed on 7 November at 5:00 PM EST: 29 hours. The Federal Register notice was published on 10 November, the same day the suspension took effect (Federal Register 2025-19839). The public only learned of the comment period because of an unofficial release on 6 November; the official notice appeared after the comment period had already closed.

Whether such truncated procedures are legally challengeable remains uncertain: the Federal Circuit ruled in September 2025 that Section 301 actions must comply with standard US administrative law requirements on public notice and comment, but USTR explicitly contests this, and importers filed a petition on 20 February 2026, the day of the IEEPA ruling, asking the Supreme Court to settle the matter.

USTR Ambassador Jamieson Greer confirmed on 20 February 2026, the day of the Supreme Court ruling, that the administration would initiate several new Section 301 investigations covering 'most major trading partners.' He has reiterated this intent on US news media repeatedly since then. The legal mechanism has changed, but the bilateral pressure cooker has not cooled.

* For automobiles, the Section 232 tariff applies to the full customs value. For steel and aluminium derivatives, the tariff applies only to the metal content share, not the full customs value. Products subject to Section 232 may also face IEEPA or Section 122 tariffs on the non-metal share. We report trade values of products affected by deal rate modifications but do not estimate underlying tariff relief.

** Some derivative products are subject to both steel and aluminium Section 232 tariffs. We assign overlapping products to steel. Total trade in products subject to any aluminium tariff, including those counted under steel, is $100 billion; the $30 billion shown excludes products already counted under steel. All figures are total customs values of affected products.