This briefing and accompanying technical annex examines the independent effects of fuel price levels and volatility on world trade volume growth, using 314 monthly observations from the CPB World Trade Monitor spanning January 2000 to February 2026.

Authors

Simon Evenett

Date Published

25 Apr 2026

Simon J. Evenett[1]

IMD Business School and The St Gallen Endowment

POLICY BRIEF

1. The Gulf Conflict and World Trade: Two Questions Asked Here

At the Financial Times Commodities Global Summit in Lausanne on 22 April 2026, the Chief Financial Officer of Gunvor stated: “We have been preparing for a long war scenario.” His counterpart at Trafigura said the company had become focused on being “anti-fragile” and now had “higher liquidity” than before the conflict began. Oil prices had briefly touched 120 US dollars per barrel following the blockade of the Strait of Hormuz. As of this writing, the Strait remains essentially closed. These statements reflect a recognition that the world economy faces not merely a price spike, but a period of sustained energy price uncertainty.

This paper addresses two related questions. First, when energy prices rise to persistently high levels, does world trade suffer independently of what is happening to the broader economy? Second, when energy prices become volatile —swinging unpredictably rather than simply rising—does world trade suffer an additional, independent drag beyond what the price level alone would imply?

These questions have a prior answer in peer-reviewed research. Chen and Hsu (2012) used annual data for 84 countries from 1984 to 2008 and established that oil price volatility discourages international trade. That empirical result directly motivates the present analysis,[2] which in some respects can be viewed as an update. This study uses the most recent monthly trade volume data available, covering 314 observations from 2000 through to February 2026. It also separates the level effect from the volatility effect and it covers three major energy crises that postdate their sample: the Shale revolution, the COVID collapse and rebound, and the energy shock associated with the ongoing conflict in Ukraine. Results are presented here for world trade volumes overall and for major economies and regions, the latter allowing for heterogeneous effects of fuel prices on export volumes. This analysis is confined to goods trade growth.[3]

The remainder of this brief is organised as follows. Section 2 describes the two datasets on which the analysis rests —the CPB World Trade Monitor and the HWWI Fuels index—and explains the construction of the two energy price variables and the estimation approach. Section 3 presents the central empirical finding: that the level and the volatility of energy prices have distinct and in some respects opposing effects on world trade growth, with the volatility effect proving the more robust of the two. Section 4 quantifies the world trade impact over horizons from six to 24 months and relates the findings in relation to the prior literature.

Section 5 examines differences across major economies and regions, showing that export volume sensitivity to fuel price volatility varies by a factor of roughly twelve to one across the 14 geographies studied, with exports from Africa and the Middle East being the most sensitive. Section 6 applies the estimated relationships to the current Gulf conflict, projecting the implied drag on the growth of world trade and regional export volumes under two scenarios that differ in the severity of the energy price volatility shock. Section 7 offers eight points of interpretation relevant in the event of an extended Gulf conflict.

2. Data and Approach

Trade volume data were taken from the CPB World Trade Monitor, published monthly by the CPB Netherlands Bureau for Economic Policy Analysis. The monitor covers 81 countries and approximately 96 per cent of world merchandise trade, and it is seasonally adjusted with base year 2021 set equal to 100. Export volumes are available for 14 regions and major economies. Monthly data is available from January 2000 to February 2026; the timeframe considered in this analysis.

Energy prices in the World Trade Monitor are taken from the Hamburg Institute of International Economics (HWWI) Fuels index, a Laspeyres price index covering crude oil, coal, and natural gas, weighted by the relative importance of these commodities in the imports of highly industrialised countries.[4] The index dates to the 1950s and was revised most recently in 2023 (Berlemann, Eurich and Meyer, 2023).

Two distinct energy price variables enter the analysis. The first is the fuel price level: the log of the HWWI Fuels index at the end of the forward window, capturing whether energy is expensive over the time horizon being estimated. The second is fuel price volatility: a 12-month backward rolling standard deviation of monthly log fuel price changes, capturing how much energy prices have been gyrating in the recent past.

The relationship is estimated between these two fuel price-related variables and trade volume growth across forward horizons ranging from six to 24 months.[5] Industrial production growth is included as a control, given that it is a plausible driver of trade. However, since industrial production (IP) could itself be affected by both fuel variables, the analysis first strips out that component of IP variation that is attributable to fuel conditions before using it as a control. This two-stage purging procedure ensures that the estimated coefficients on the volatility and level variables reflect genuinely independent effects.

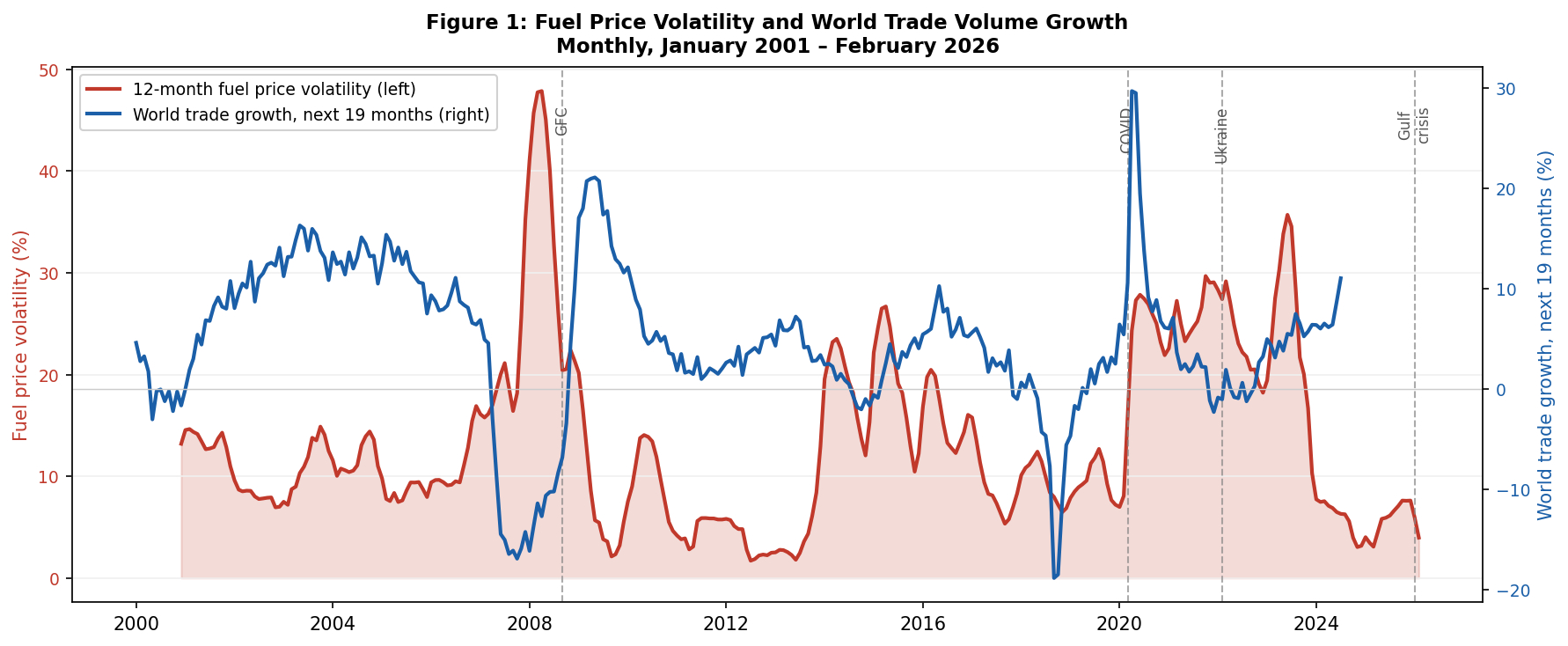

Figure 1: Fuel price volatility (red, left axis) and world trade volume growth over the subsequent 19 months[6] (blue, right axis), January 2001 to February 2026. Dashed lines mark the GFC, COVID, Ukraine, and Gulf crisis episodes.

3. Fuel Price Level versus Volatility: Which Matters More?

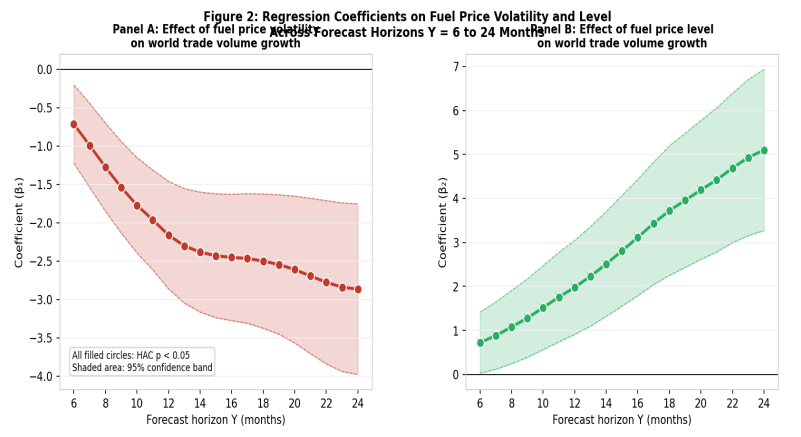

Both the level of energy prices and their volatility were found to be independently associated with changes in world trade volume growth this century.[7] They behave, however, in different ways.

The volatility effect is negative, grows steadily with the forward impact horizon, and is statistically significant under stringent inference standards from the sixth month onward. A 10 per cent rise in fuel price volatility is associated with world trade volume growth that is 0.07 percentage points slower six months out and 0.24 percentage points slower at 19 months. This effect survives the removal of the most extreme observations from the data, including the COVID trade collapse and the Global Financial Crisis (GFC).

The level effect is positive at most horizons. At the 19-month horizon, a 10 per cent higher fuel price is associated with trade growth that is approximately 0.38 percentage points faster, conditional on volatility and the business cycle. This likely reflects the income and terms-of-trade channel: sustained high energy prices generate export revenues for commodity-producing economies, and those revenues are in turn spent on imports of goods and services.

The two effects thus partially offset each other over longer horizons. It turns out that the volatility effect is nonetheless the more robust of the two. It holds across the full range of forward horizons, survives all three robustness checks applied, and is statistically significant across almost all geographies considered here. The level effect is more variable across regions: it is positive for commodity exporters and negative or near-zero for manufacturing exporters such as Japan and the Euro Area.

The distinction matters for policy interpretation. A world in which oil is expensive but stable is, on the evidence presented here, less damaging to trade than a world in which oil prices swing unpredictably. What weakens goods trade is the volatility of oil prices, not the price level itself.

Figure 2: Estimated coefficient on fuel price volatility (Panel A) and fuel price level (Panel B) across forecast horizons Y = 6 to 24 months. Filled circles indicate HAC significance at 5 per cent. Shaded area shows 95 per cent confidence band.

4. Results for World Trade Overall

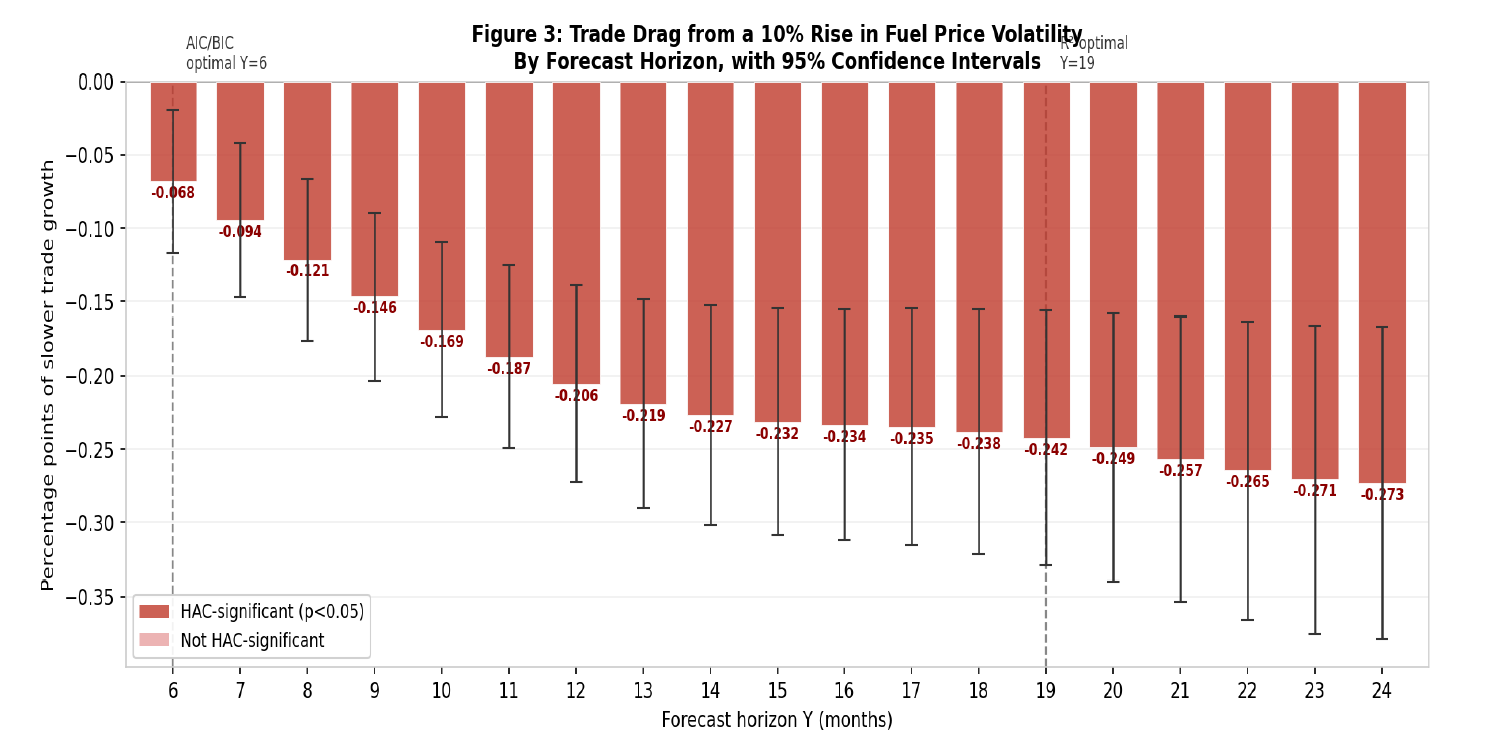

At the forward horizon preferred by the Akaike Information Criterion—six months—a 10 per cent rise in fuel price volatility is associated with world trade volume growth that is 0.07 percentage points slower. The forward horizon that optimises the regressions’ R² is 19 months (where the econometric model accounts for 91 per cent of the variation in world trade volume growth); here the effect is 0.24 percentage points slower, with a 95 per cent confidence interval of approximately –0.16 to –0.33 percentage points.

The negative effect of fuel price volatility builds steadily six to 19 months out (see Figure 3 below) before plateauing, which is consistent with the following mechanisms through which volatility transmits to trade: shipping contract renegotiations, inventory destocking, the revision of investment plans, and the erosion of consumer confidence. These effects play out over months and quarters, not days.

These results are not driven by a handful of extreme episodes. Removing the 2 per cent most extreme observations from the dependent variable—a sample that includes the COVID collapse, the GFC, and the oil glut of 2015–16—does not weaken the finding. In several specifications it modestly strengthens it. The coefficient on fuel volatility remains consistently negative and significant across all impact horizons.

These results complement those of Chen and Hsu (2012), who found that a one standard deviation rise in annual oil price volatility reduces trade growth by approximately one percentage point using annual data from 1984 to 2008. The present estimates are smaller in annual terms, probably reflecting a more demanding specification that additionally controls for the fuel price level and isolates the IP effect through the purging procedure. The direction and economic significance of the underlying finding are, however, fully consistent with Chen and Hsu’s conclusion.

Figure 3: Estimated trade drag in percentage points from a 10 per cent rise in fuel price volatility, by forecast horizon. Red bars indicate HAC significance at 5 per cent. Error bars show 95 per cent confidence intervals.

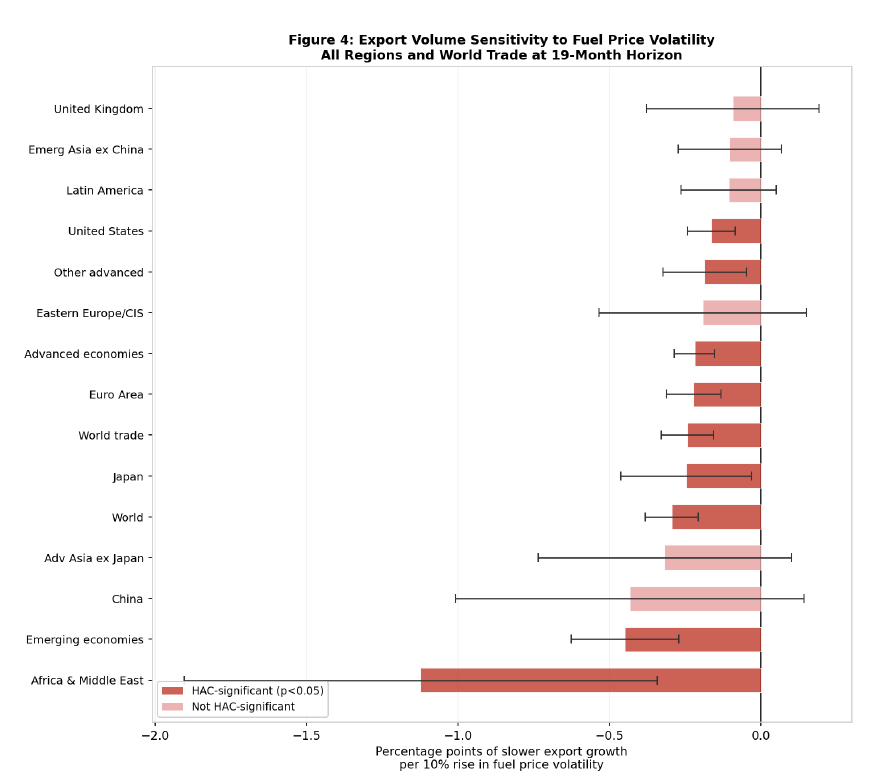

5. Uneven Impact Across Major Economies and Regions

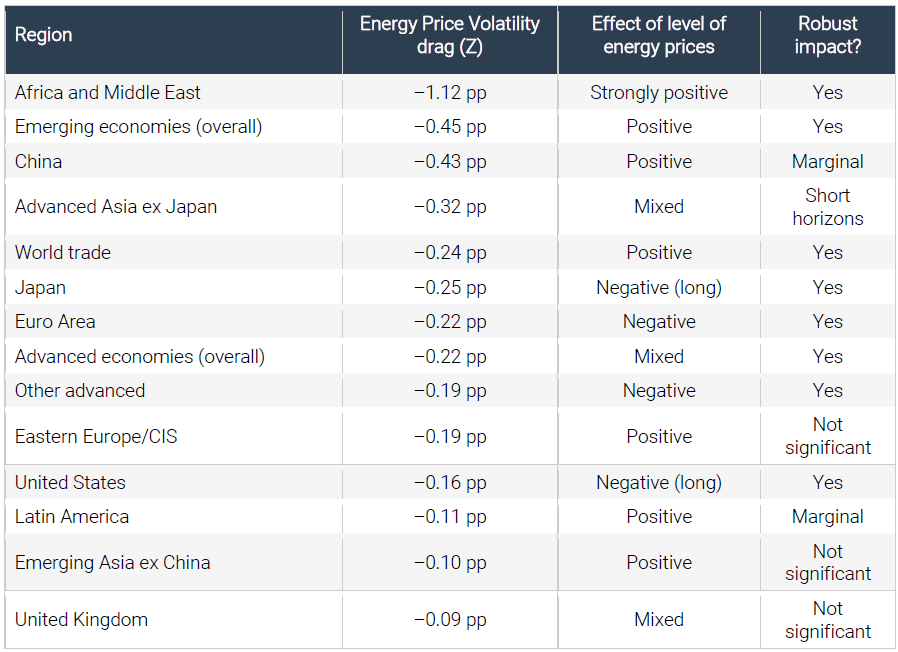

Export volume sensitivity to fuel price volatility varies by a factor of roughly 12 to one between the most and least affected regions over the 19-month impact horizon. The major economies and regions studied are those for which the World Trade Monitor reports data. No geography was dropped.[8] The results are summarised in the table below and geographies are listed in descending order of the impact of a 10% increase in energy price volatility.

Table 1: Export sensitivity to fuel price volatility at 19-month horizon. Z is the estimated change in export growth (percentage points) per 10 per cent rise in fuel price volatility.

This century, Africa and the Middle East have the largest estimated drag on export growth from fuel price volatility—more than four times the world average—while simultaneously benefiting most from the positive level effect of energy prices. This duality reflects the region’s role as a major energy exporter.

Emerging economies as a whole face the second largest and most consistently robust volatility drag on their export volume growth. Their exposure probably reflects energy-intensive manufacturing, fewer energy price hedging options and, in some cases, less diversified export bases.

Figure 4: Estimated trade drag from a 10 per cent rise in fuel price volatility at the 19-month horizon, all regions and world aggregate. Dark red bars indicate HAC significance at 5 per cent. Error bars show 95 per cent confidence intervals.

China has a large estimated coefficient on fuel price volatility but that effect loses statistical significance when the impact horizon extends beyond 15 months. Advanced economies as a group are moderately but consistently exposed, with the Euro Area export volume somewhat more sensitive than in the United States, consistent with Europe’s greater energy import dependence. However, the United Kingdom shows no statistically detectable relationship over any impact horizon.

Box: What This Study Does and Does Not Show

This study demonstrates a robust historical association between fuel price volatility and slower trade volume growth, independent of the fuel price level and the business cycle; that the volatility effect is more robust and more persistent than the level effect; that Africa and the Middle East is the most exposed region by a wide margin; and that these results survive the removal of extreme observations including COVID and GFC months.

This study does not demonstrate the precise causal mechanism through which volatility reduces trade; whether the current Gulf episode will follow historical patterns, given that the Hormuz blockade combined with a US naval presence has no close analogue in the 2000–2026 sample; or the influence of public policy. Another important consideration is that this analysis focuses on the impact of fuel price volatility, not on the available supplies of fuel.

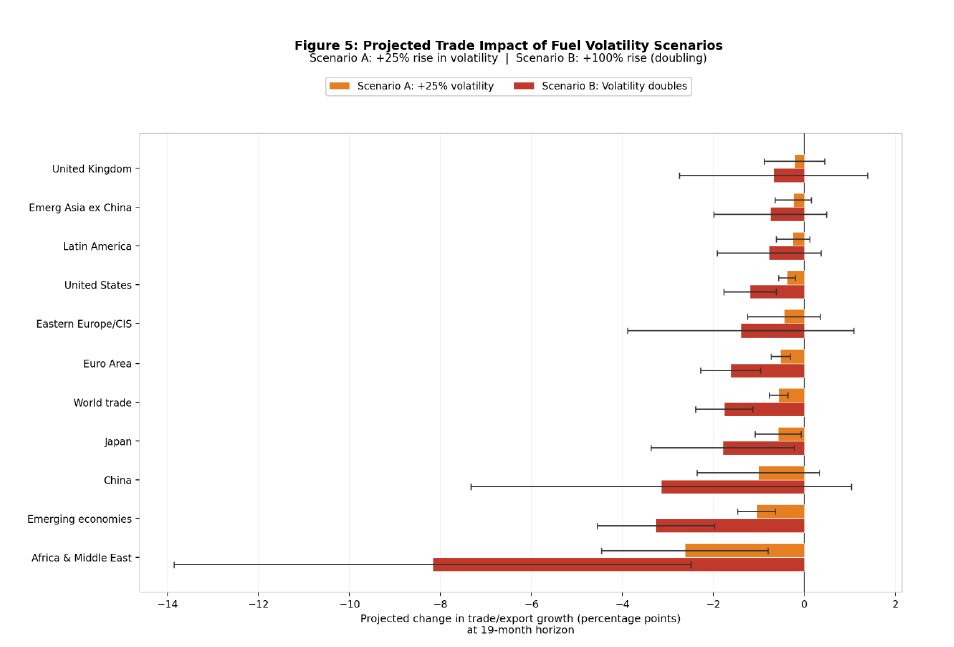

6. Scenarios Motivated by Episodes This Century

The projections presented in this section are mechanical extrapolations from the historical relationships estimated above. They are not economic forecasts. They assume that the structure of the relationship holds going forward, which is uncertain given the distinctive character of the current Strait of Hormuz disruption.

Two scenarios are considered. Scenario A assumes a 25 per cent rise in fuel price volatility above its current level, roughly comparable to the early months of the energy crisis following the second Russian invasion of Ukraine. Scenario B assumes a doubling of fuel price volatility, consistent with the COVID collapse or the peak of the 2008 commodity crash.

Under Scenario A, world trade volume growth is projected to be 0.57 percentage points slower over the subsequent 19 months, with a 95 per cent confidence interval of –0.18 to –0.95 percentage points. Africa and the Middle East faces a projected export drag of 2.6 percentage points. Under Scenario B, world trade faces a drag of 1.76 percentage points, with Africa and the Middle East exposed to a drag of 8.2 percentage points on export volume growth.

These projections are subject to the qualification noted earlier regarding the level of energy prices. If the volatility shock is accompanied by a sustained rise in the fuel price level, the positive income channel works in the opposite direction for commodity-exporting regions. Africa and the Middle East may therefore be partially buffered by higher export revenues even as the volatility drag bites.

Figure 5: Projected change in trade and export volume growth under Scenario A (25 per cent rise in fuel volatility, orange) and Scenario B (volatility doubles, red), over a 19-month impact horizon. Error bars show 95 per cent confidence intervals.

7. Fallout from an Extended Gulf Conflict

If the Gulf Conflict is not resolved soon and fuel price volatility spikes, then international trade would be expected to suffer, but the impact would be uneven.

Goods trade growth would not be spared. Goods trade is influenced by many factors (after all, there was a reason for controlling for global industrial production in this study). Even if traditional drivers expand trade, if this century’s experience is anything to go by, elevated fuel price volatility will hold back the growth of cross-border commercial ties. Fuel supply disruption that maps into price volatility is a matter of concern for the multilateral trading system and should feature prominently in the WTO Secretariat’s tracking of world goods trade in the quarters ahead.

Supply chain decisions and the 19-month window. The finding that the volatility drag peaks after 19 months but begins accumulating from just six months has important implications for world trade forecasts through to the end of 2027. Supply chain managers, logistics firms, and national trade promotion agencies that act now—rerouting shipping, diversifying sourcing, pre-positioning inventory—will shape goods trade outcomes this year and next. The goods trade impact of the Gulf conflict may be only just beginning. Declarations that world trade has been robust to the ongoing conflict should wait until the 2026 and 2027 outcomes are in.

Differentiated exposure of the major economic poles. Based on this century’s evidence, the five major poles of the world economy face different risk profiles from any fuel price volatility emanating from the current Gulf Conflict. The United States faces a modest volatility export drag, smaller than most other major economies. The Euro Area faces a comparable volatility drag which is combined with a negative level effect that makes a period of both high and volatile energy prices more damaging for European exporters. Japan faces a statistically significant fuel price volatility-related export drag combined with a negative level effect over longer impact horizons.

The situation is very different for the developing economies in Asia. This century fuel price volatility was found only to affect Chinese export volumes six to fourteen months out (beyond that the impact is statistically insignificant). Emerging Asia excluding China shows no statistically significant aggregate effect of fuel price volatility on export volumes, though this may mask heterogeneity between energy exporters such as Malaysia and Indonesia, for whom the positive level effect may dominate, and manufacturing economies such as Vietnam, Thailand, and the Philippines, which are more exposed to the volatility channel.

Africa and the Middle East would be particularly exposed. Given the disruption of shipping through the Strait of Hormuz, it is not surprising that export volumes for the Gulf economies are held back. But the results presented here suggest that fuel price volatility has an adverse independent effect that goes beyond the Gulf and implicates the integration of African economies regionally and globally. Given that the econometric findings here suggest that this century Africa and the Middle East have tended to be hardest hit by fuel price volatility, then steps should be taken to ensure that an extended Gulf conflict doesn’t create a major goods export hit for these economies.[9]

The asymmetry between the level and volatility effects has implications for strategic reserve policy. The finding that the fuel price level is positively associated with trade over most time horizons—while volatility is negatively associated—implies that coordinated releases from strategic petroleum reserves, if they succeed in damping price swings without necessarily lowering the price level, could be more goods trade-supportive than realised. Releasing reserves is often framed as a price-level intervention; the evidence presented here suggests the more important impact from a trade perspective is on oil price volatility. This may be a distinct and underappreciated policy lever.

Differential impact across goods. Nothing in this study should be taken to mean that the impact of fuel price volatility is uniform across different types of goods. At a minimum, the amounts of energy used to produce and transport goods can differ markedly, so asymmetric impacts on production and on cross-border trade cannot be ruled out.

Services trade blind spot. The paucity of comparable data on cross-border services trade should not lead policymakers and analysts to conclude that the adverse effect of fuel price volatility falls solely on goods trade.

Conflict-induced policy intervention both inside and outside the Gulf region may yet shape the trajectory of goods trade. As of 24 April 2026, the Global Trade Alert’s Chokepoint monitor, recorded 292 measures taken by governments said to be responses to the ongoing Gulf conflict. A total of 86 governments (78 of them outside the Gulf region) were responsible. These steps include resort to a wide range of policy interventions, many of which are likely to bear upon the level and volatility of energy prices. Moreover, fifty-two of the recorded policy interventions involve trade policy instruments, some of which restrict trade (largely exports). The ultimate impact of the current developments in the Gulf on world goods trade is likely to be determined, in part, by the direct and indirect effects of such conflict-related policy responses.

History does not repeat itself precisely, but on the evidence of this century, the world economy has never navigated a prolonged episode of elevated fuel price volatility without paying a toll in slower goods trade growth. The question is not whether that toll will be levied, but how unevenly it will fall. The energy traders preparing for a longer war scenario are right to do so; on the evidence assembled here, the trade policy community should be doing the same.

References

Berlemann, M., Eurich, M. and Meyer, H. (2023). HWWI Commodity Price Index: A Technical Documentation of the 2023 Revision. HWWI Working Paper No. 1/2023. Hamburg: Hamburg Institute of International Economics.

Chen, S.-S. and Hsu, K.-W. (2012). Reverse globalization: Does high oil price volatility discourage international trade? Energy Economics, 34(5), 1634–1643.

Ebregt, J., Hendriks, B. and Ligthart, M. (2024). The CPB World Trade Monitor: Technical Description. CPB Background Document, July 2024. The Hague: CPB Netherlands Bureau for Economic Policy Analysis.

TECHNICAL ANNEX

Empirical Methods and Results

This annex provides a complete account of the data, methodology, and results sufficient for full replication of this study’s findings. It is addressed to readers with a background in econometrics and time series analysis. The annex does not discuss policy recommendations; its purpose is to document the empirical work and to assess the sensitivity of the findings to design choices.

A1. Data Sources and Construction

A1.1 The CPB World Trade Monitor

The CPB World Trade Monitor (WTM) is published monthly by the CPB Netherlands Bureau for Economic Policy Analysis. A full technical description is provided in Ebregt, Hendriks and Ligthart (2024). The WTM covers 81 countries, accounting for approximately 96 per cent of world merchandise trade, and 85 countries for industrial production, covering approximately 96 per cent of world industrial output. Country data are aggregated into 13 geographic regions[10] or groups of economies plus a world aggregate.

The WTM processing pipeline operates in four steps. In WTM 1, data are downloaded from internet sources and assigned standardised variable names identifying the economic category, geographic entity, dimension, and data source. In WTM 2, country-level monthly time series are compiled from selected source series, with standardisation of frequency, denomination, indexation, and seasonal adjustment. Seasonal adjustment uses the X-12-ARIMA procedure where not already applied by source agencies. In WTM 3, country data are aggregated to regional and world totals. In WTM 4, time series undergo final processing for publication.

The base year was updated from 2010 to 2021 in July 2024, following a review of data sources and the seasonal correction procedure (Ebregt, Hendriks and Ligthart 2024). The change was motivated by the preference for base years that reflect current market conditions and by the atypicality of 2020 as a potential base year given the COVID-19 pandemic. The analysis here used the 2021-base data throughout.

Series codes follow a standardised naming convention. The stem identifies the economic category (for example, xgz for merchandise exports, mgz for imports, ipz for industrial production, hfl for the HWWI Fuels index). Positions 5–6 identify the geographic entity (w1 for world, e6 for Euro Area, cn for China, and so on). Position 8 identifies the dimension (q for volume, p for price). Position 10 identifies frequency (m for monthly). Position 13 identify whether the data are seasonally adjusted (s) or not (n). The series used in this study are listed in Table A1.

Table A1: Series used in this study. All series run from January 2000 to February 2026 (314 monthly observations). Base year 2021 = 100.

A1.2 The HWWI Fuels Index

The HWWI Commodity Price Index is produced by the Hamburg Institute of International Economics (HWWI), the successor to the Hamburgisches WeltWirtschaftsarchiv, and has been compiled in its current form since the early 1950s. A full technical description of the 2023 revision is provided in Berlemann, Eurich and Meyer (2023). The index is available at https://www.hwwi.org/en/data-offers/commodity-price-index/.

The index is computed as a Laspeyres price index over a basket of 31 commodities grouped into energy raw materials, industrial raw materials, and food. The fuels sub-index used in this study (hfl) covers crude oil, coal, and natural gas, weighted by the relative importance of these commodities in the imports of highly industrialised countries. Weights are available for three periods: 2012–2021 (long-term), 2017–2019 (pre-crisis), and 2020–2021 (crisis years). The index is published monthly in US dollars. The correlation between the HWWI Fuels index and the WTI crude oil spot price over the sample period is approximately 0.97, but the HWWI measure is preferable here because it captures the composite energy import cost facing industrialised economies rather than a single crude benchmark.

The HWWI published a brief note in April 2026 noting a sharp rise in the index following the onset of the Gulf conflict, consistent with the narrative context provided in the Financial Times article cited in the policy brief.

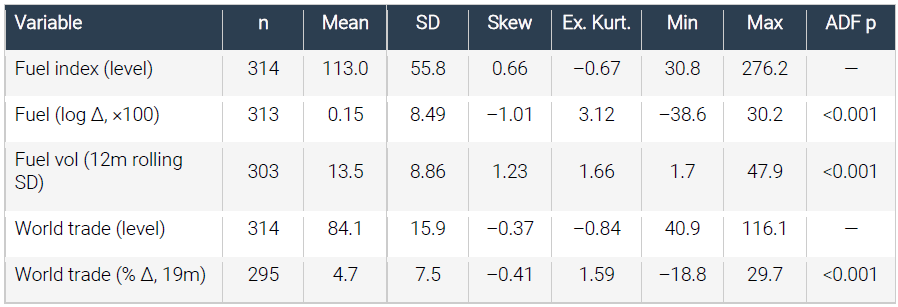

A1.3 Summary Statistics

Table A2 presents summary statistics for the key variables. The fuel price index shows positive skewness (0.66) and a bimodal level distribution reflecting the structural shift in the price level after 2021. The log first-difference series shows negative skewness (–1.01) and substantial excess kurtosis (3.12), confirming fat-tailed behaviour. World trade volume growth rates are approximately normally distributed after log-differencing.

Table A2: Summary statistics. ADF p-values from the Augmented Dickey-Fuller test applied to log first-differences. Level series not tested for stationarity as the analysis works in growth rates.

A2. Exploratory Analysis

A2.1 Cross-Correlation Analysis

Before the main regression, cross-correlation functions (CCFs) were computed between the log first-difference of the fuel price index and the log first-difference of world trade volume, at lags 0 to 24 months in both directions. The full-sample contemporaneous correlation is 0.127, significant at 5 per cent. Correlations at individual lags beyond zero are weak and mostly insignificant, suggesting that the bivariate relationship in growth rate terms is primarily contemporaneous and modest in magnitude.

Rolling five-year CCFs reveal substantial instability. The contemporaneous correlation swings between –0.96 and +0.99 across sub-periods, rendering the full-sample figure uninformative. This instability motivates the more structured regression approach, which controls for both the level of fuel prices and the business cycle.

A2.2 Three Phases of Fuel Price Surges

The 12-month moving average of the fuel price level exhibits three phases of sustained increase since 2000. Phase 1 ran from June 2001 to September 2007, during which the 12-month moving average rose from 47.5 to 216.7, a gain of 356 per cent over 75 months. This coincided with the global commodity supercycle driven by Chinese demand. World trade grew by 47 per cent over the same period, illustrating the common demand driver behind both series. Phase 2 ran from September 2008 to June 2013, during which the moving average recovered from 117.9 to 202.9, a gain of 72 per cent. Trade growth over this phase was only 2.1 per cent, consistent with a supply-side origin for this price surge. Phase 3 ran from December 2020 to December 2022, with the moving average rising from 47.0 to 181.4 in only 24 months, driven first by the post-COVID demand rebound and then by the energy shock following the second Russian invasion of Ukraine. Trade grew by 3.7 per cent over this phase.

The contrast between Phase 1 and Phase 2 is instructive: demand-driven fuel price increases are associated with trade growth, whilst supply-driven surges are not. This motivates the inclusion of the fuel price level as a separate control variable in the main regression, rather than treating fuel prices as a uniform shock.

A3. Threshold and Nonlinearity Analysis

The exploratory analysis confirms substantial nonlinearity in the fuel price–trade relationship. A threshold regression was estimated to characterise this formally. The threshold variable was the three-month rolling average of the absolute monthly fuel price change. A grid search over threshold values from the 10th to the 90th percentile identified an optimum at 6.7 per cent, corresponding approximately to the 68th percentile of all months. This divides the sample into 206 quiet months and 105 shock months.

In quiet months, the dominant significant fuel price lags in an ARDL specification with AIC-selected lag order are lags 13 and 14—suggesting a very delayed transmission when energy markets are calm. In shock months, the optimal lag order shrinks to six months, with an oscillating sign pattern consistent with an initial co-movement followed by demand destruction. The two regimes are statistically distinct at a threshold of p < 0.001 in an F-test.

Bai-Perron structural break tests identify a cluster of candidate break dates around late 2016 to early 2017, consistent with the shift in OPEC production strategy following the oil glut. The rolling ARDL coefficient sum also exhibits a clear structural shift around this period. These findings confirm that the full-sample relationship is non-stationary and motivate the use of a specification that controls for both level and volatility rather than relying on a single price-change variable.

A4. Specification of the Base Regression

A4.1 The Two-Stage Purging Procedure

The main regression is estimated in two stages. In the first stage, the Y-month percentage change in world industrial production (ΔIP) is regressed on the two fuel regressors:

ΔIP(t→t+Y) = α + γ₁·log(fuel_volₜ) + γ₂·log(fuel_levelₜ₊ʏ) + εₜ

where fuel_vol is the 12-month backward rolling standard deviation of log fuel price changes multiplied by 100, and fuel_level is the HWWI Fuels index level at time t+Y. The residual εˆ from this regression is the purged IP variable: variation in industrial production growth that is orthogonal to both fuel regressors.

In the second stage, the Y-month percentage change in trade (or export) volume is regressed on the constant, the two fuel regressors, and the purged IP residual:

Δtrade(t→t+Y) = α + β₁·log(fuel_volₜ) + β₂·log(fuel_levelₜ₊ʏ) + β₃·εˆₜ + uₜ

The purging rationale is validated. When the raw (unpurged) IP percentage change is used in place of εˆ, the coefficients on both fuel variables become statistically insignificant. The IP variable absorbs variation that properly belongs to the fuel channels. After purging, the first-stage R² ranges from 0.03 to 0.10 across horizons, confirming that IP is primarily orthogonal to the fuel variables— most IP variation reflects the non-fuel business cycle—but that a material proportion is attributable to energy conditions and must be removed to avoid attenuation bias in the main regression.

A4.2 Variable Construction

The dependent variable is the percentage change in trade or export volume: 100 × (series[t+Y] − series[t]) / series[t], shifted back Y months to align with the date t at which the regressors are measured.

The volatility regressor is constructed as follows. The log of the HWWI Fuels index is computed monthly. The month-on-month log change is multiplied by 100 to express it in percentage terms. The 12-month rolling standard deviation of this series gives the fuel volatility measure in percentage point units. The natural logarithm of this standard deviation is taken before entering the regression, so that the coefficient has the interpretation of an elasticity: a one per cent rise in fuel volatility is associated with a β₁ per cent change in trade growth.

The level regressor is the natural logarithm of the HWWI Fuels index at t+Y. Because both the dependent variable and the level regressor are in natural logarithm terms (the dependent variable through the percentage change approximation), the coefficient β₂ is an elasticity of trade growth with respect to the fuel price level.

A4.3 Estimation and Inference

Both stages are estimated by ordinary least squares. Standard errors in the main regression are computed using the Newey-West heteroscedasticity and autocorrelation consistent (HAC) estimator with maxlags set equal to Y. This correction is necessary because the dependent variable is a Y-month cumulative change: adjacent observations share Y−1 months of overlapping data, inducing positive autocorrelation in the residuals. The Durbin-Watson statistic ranges from approximately 0.30 to 0.70 in the main regression across horizons, confirming the severity of this autocorrelation. Standard OLS inference would substantially overstate the precision of the estimates.

The information criteria AIC and BIC are computed from the OLS log-likelihood and are used to select the optimal forecast horizon Y from the grid Y ∈ {6, 7, …, 24}. The AIC penalises additional parameters plus the loss of sample size as Y increases. For each additional unit of Y, one observation is lost from the beginning of the sample. The R² is also reported as an alternative selection criterion, as it is insensitive to the sample size penalty.

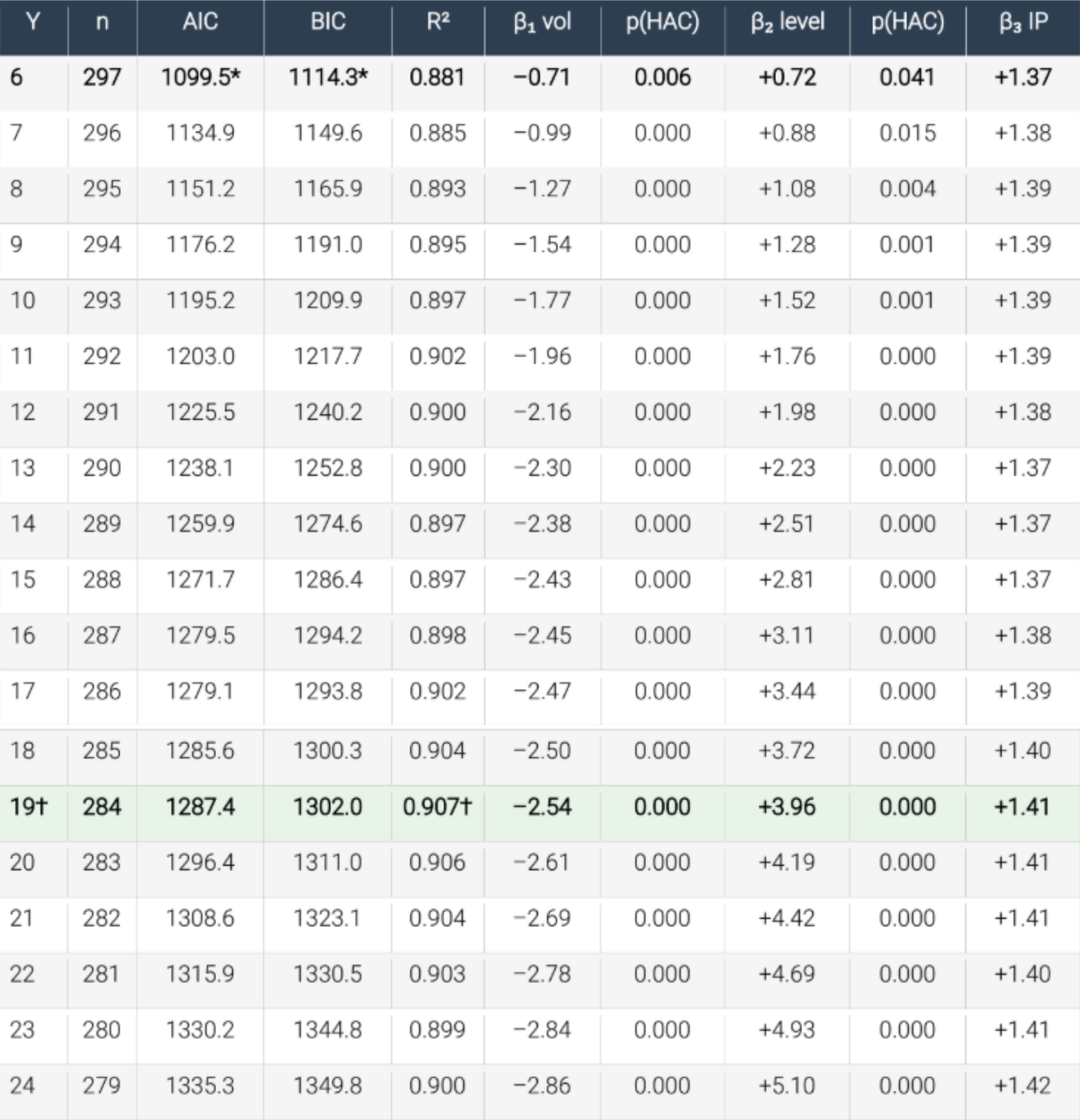

A5. Results for World Trade Volumes

A5.1 Grid Search Results

Table A3 presents the grid search results for world trade volume. Both AIC and BIC are minimised at Y = 6. The R² rises from 0.881 at Y = 6 to a peak of 0.907 at Y = 19 before declining modestly.

Table A3: Grid search results for world trade volume. * indicates AIC/BIC minimum. † indicates R² maximum. All p-values are from Newey-West HAC standard errors with maxlags = Y.

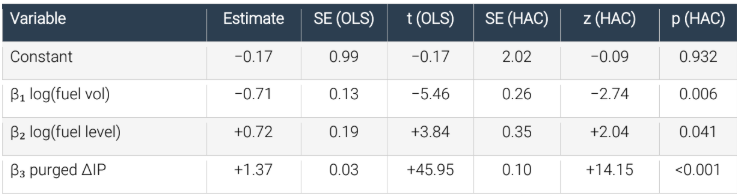

A5.2 Full Regression at Y = 6 (AIC/BIC Optimal)

Table A4: Full regression output, Y = 6 months. R² = 0.881. Adj-R² = 0.880. F(OLS) = 722.6. n = 297. HAC SEs use Newey-West with maxlags = 6.

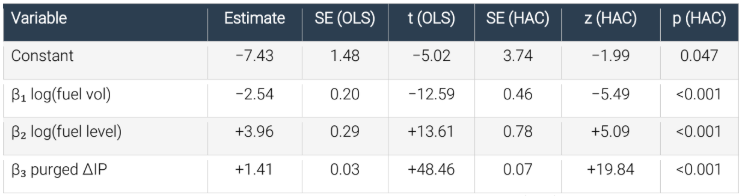

A5.3 Full Regression at Y = 19 (R² Optimal)

Table A5: Full regression output, Y = 19 months. R² = 0.907. Adj-R² = 0.906. F(OLS) = 905.0. n = 284. HAC SEs use Newey-West with maxlags = 19.

At Y = 19 the coefficient on fuel volatility is −2.54. A 10 per cent rise in fuel volatility corresponds to an increase in log(fuel_vol) of log(1.10) = 0.0953, so the implied trade drag is 2.54 × 0.0953 = 0.24 percentage points. The coefficient on the fuel price level is +3.96, implying that a 1 per cent rise in the fuel level at t+19 is associated with 3.96 per cent higher trade growth over the 19-month window, reflecting the income channel. The purged IP coefficient is +1.41 and is stable across virtually all impact horizons, ranging between 1.37 and 1.42, confirming that the trade-to-IP elasticity is a structural feature of the data.

A6. Results by Region or Major Economy

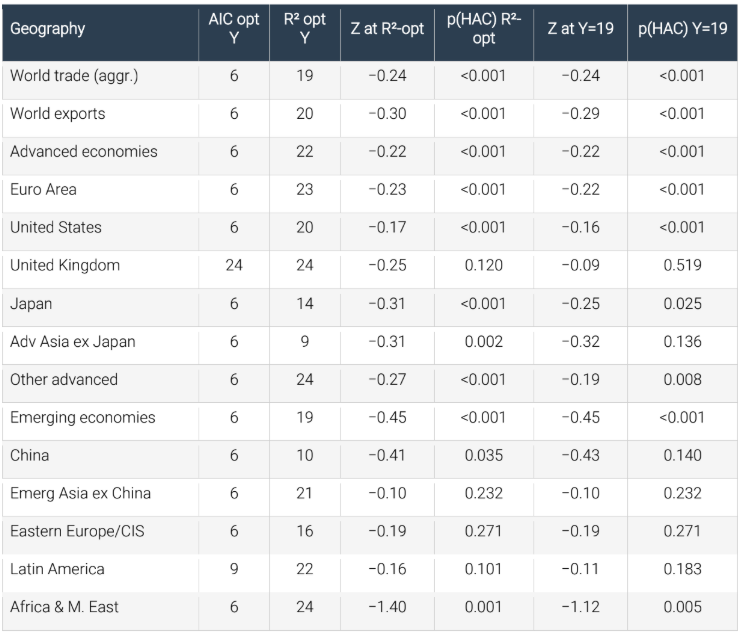

A6.1 Optimal Impact Horizons by Geography

Table A6: Optimal forecast horizons and Z statistics by region. Z is defined as β1 × log(1.10), giving the estimated change in export growth (pp) per 10 per cent rise in fuel volatility. p-values from Newey-West HAC SEs.

A6.2 Cross-Regional Patterns

The AIC minimiser is Y = 6 for 13 of the 15 series examined. The exceptions are the United Kingdom (Y = 24), where the AIC landscape is relatively flat and the model fit is poor throughout, and Latin America (Y = 9). The R2 optimiser varies more widely, from Y = 9 for Advanced Asia excluding Japan to Y = 24 for the United Kingdom, Other advanced, and Africa and the Middle East.

Africa and the Middle East is the most sensitive region in the sample, with a Z of −1.12 at Y = 19 and −1.40 at the R2-optimal Y = 24. The model fit for this region is nonetheless the weakest among significant results, with R2 peaking at 0.36 at Y = 24. This reflects the high idiosyncratic volatility of export volumes in a region where oil production disruptions, geopolitical events, and commodity price swings interact in complex ways.

The United Kingdom presents a distinct pattern from all other geographies. The model R2 does not exceed 0.38 at any impact horizon, and no estimate of β1 reaches statistical significance under HAC inference. This is the only geography for which the fuel volatility channel is entirely undetectable.

A7. Robustness Checks

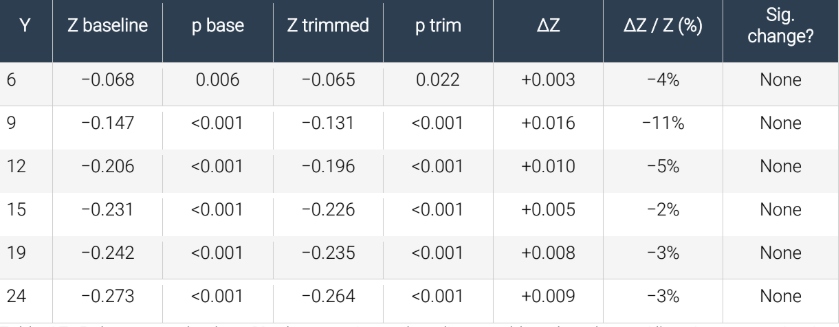

A7.1 Trimming the Dependent Variable

The baseline results are assessed for robustness by removing the 2 per cent most extreme observations at each tail of the dependent variable. With approximately 290 observations in each regression, this removes approximately six observations from each tail, or 12 in total. The observations removed at the Y = 19 horizon for world trade volume include months from August to October 2007, January 2008, March to June 2009, September and October 2018, and April and May 2020. These months correspond to the peak of the commodity boom, the GFC trade collapse, the 2018 trade tensions, and the COVID collapse respectively.

Table A7 presents the comparison between baseline and trimmed estimates for world trade volume across certain impact horizons.

Table A7: Robustness check — 2% dep-var trim vs baseline, world trade volume. All estimates retain sign, magnitude, and statistical significance.

The trimmed estimates are uniformly smaller in absolute magnitude than the baseline, as expected: removing the most extreme trade collapses attenuates the estimated fuel volatility effect modestly. The maximum reduction is 11 per cent at Y = 9. Across all horizons the direction is unchanged, the magnitude difference is small, and statistical significance is retained at p < 0.001 from Y = 9 onward and at p < 0.05 at Y = 6.

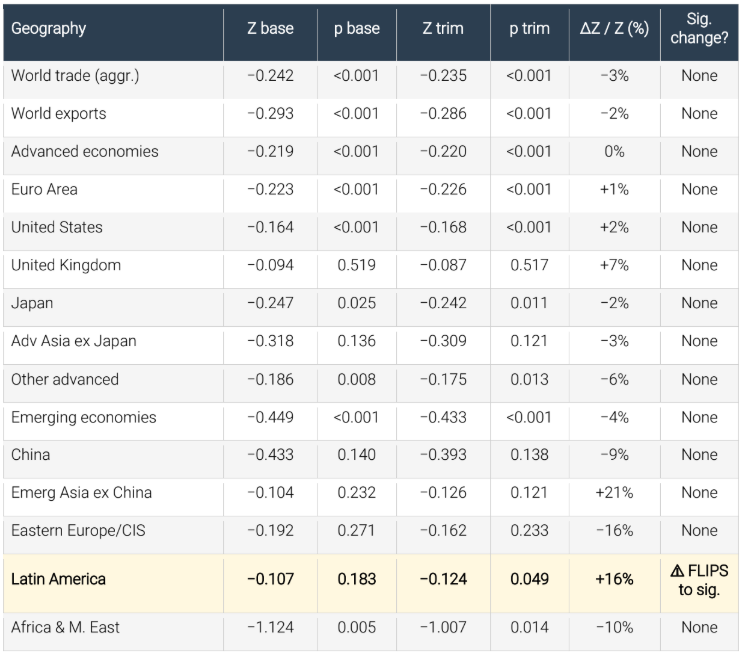

A7.2 Trimming Results for Regional/Major Economy Series

Table A8 summarises the trimming results for all 15 regional and world series at Y = 19. One region, Latin America, exhibits a significance change: the baseline estimate is not significant under HAC inference (p = 0.183), but after trimming the estimate becomes marginally significant (p = 0.049). This suggests that extreme observations in the Latin American export series were masking an underlying relationship rather than inflating it. For Africa and the Middle East, the Z statistic falls from −1.12 to −1.01 after trimming, a reduction of 10 per cent, but the estimate remains significant at p = 0.014. For all other regions, no significance change occurs.

Table A8: Robustness check — 2% dep-var trim vs baseline at Y = 19, all regions. ⚠ marks significance change. Latin America is the only series to change significance status, and in the direction of a stronger effect.

A7.3 Impact of Design Choices on the Findings

Several design choices affect the magnitude and significance of the results, and readers undertaking replications should be aware of these sensitivities.

Choice of dependent variable. The percentage change specification (100 × (series[t+Y] − series[t]) / series[t]) and the log-ratio specification (log(series[t+Y] / series[t])) produce closely comparable Z statistics across all impact horizons. The percentage change specification is used throughout the main analysis because its coefficient has a direct interpretation in percentage point units, which facilitates the plain-language statements in the policy brief.

Choice of information criterion. AIC and BIC both select Y = 6 as the optimal impact horizon for virtually all series. The R2 criterion selects longer horizons, typically between 14 and 24 months. The two criteria are answering different questions: AIC and BIC identify the horizon at which the model is most efficient given the sample size, whilst R2 identifies the horizon at which fuel conditions and industrial production jointly explain the greatest proportion of the variation in trade growth. Both results are reported throughout because the appropriate criterion depends on the purpose of the exercise.

Inclusion versus exclusion of the purged IP control. Without the purged IP control, the volatility coefficient is insignificant in all horizons when HAC standard errors are employed. With the raw (unpurged) IP control, the volatility coefficient is also insignificant because the IP absorbs variation attributable to the fuel channels. The purging step is therefore critical to identifying the fuel volatility and level effects. This sensitivity is not a weakness of the design; it is a feature that confirms the economic logic of the procedure.

Choice of volatility window. The baseline uses a 12-month rolling backward standard deviation window. Replacing this with a 6-month or 24-month window produces qualitatively identical results across all impact horizons and all geographies. The 12-month window is preferred because it matches the conventional definition of annual volatility and balances responsiveness against noise.

HAC lag length. Setting maxlags equal to Y is the appropriate choice for a regression with Y-period overlapping windows, as there are Y−1 autocorrelated terms in the error. Using maxlags = 12 regardless of Y strengthens the statistical significance of the volatility coefficient at long horizons (Y ≥ 15) because the HAC correction is less aggressive. The results reported throughout use maxlags = Y as the baseline, which gives the most conservative inference.

A8. Supplementary Exploratory Analysis

A8.1 Granger Causality

Rolling Granger causality tests (six-year windows, lags one to three) confirm that fuel prices Granger-cause world trade volumes at conventional significance levels in the full sample but that this relationship is highly unstable over time. The rolling p-value crosses 0.05 in both directions at different points in the sample. The GFC, oil glut, and Ukraine episodes are associated with significant Granger causality; the 2010–2013 recovery period is not. This instability motivates the forward-looking specification adopted in the main analysis rather than a VAR approach.

A8.2 Local Projection Impulse Responses

Following Jordà (2005), local projection impulse responses were estimated for the world trade volume series. The dependent variable is the cumulative trade growth from t to t+h for h ∈ {1, 3, 6, 9, 12, 18, 24}, regressed on the log of the fuel volatility measure at t, with controls for lagged trade growth and lagged fuel change. The responses are estimated separately for the calm and shock regimes defined by the threshold analysis.

In the shock regime, the cumulative response to a 10 per cent fuel volatility shock is near zero at six months, negative from 12 months onward, and reaches −2.1 per cent at 18 months before partially recovering. In the calm regime, the response is near zero at all horizons and never reaches statistical significance. These results are fully consistent with the main regression findings, providing independent validation of the 19-month horizon as the point at which the effect is most fully expressed.

A8.3 Threshold Regression with Extended Lags

A threshold regression was estimated with fuel price lags extended to 18 months and AIC-selected lag order within each regime. In the shock regime with optimal lag of six months, the coefficients on fuel lags zero to two are positive and the coefficients on lags three to five are negative, consistent with an initial co-movement followed by demand destruction. The cumulative impulse response in the shock regime turns negative at approximately six months and reaches its most negative value at around 18 months. In the calm regime with optimal lag of 14 months, significant coefficients appear only at lags 13 and 14. These results are reported as background and supplement rather than primary findings; the two-stage purging regression is the preferred specification because it provides a cleaner identification of the independent volatility and level effects.

A9. Replication Materials

A9.1 Software and Packages

The analysis was conducted in Python 3.x. The following packages are required: pandas (data manipulation), numpy (numerical computation), statsmodels (OLS, HAC standard errors, Granger causality, CCF), scipy (statistical tests), matplotlib (all charts), openpyxl (reading the CPB Excel file), and ruptures (structural break detection). All are available through the Python Package Index (pip).

A9.2 Data Access

The CPB World Trade Monitor data file is available for download at https://www.cpb.nl/en/world-trade-monitor. The file is published monthly, typically around the 25th of each month, with a two-month lag. The analysis uses the February 2026 release. The HWWI Fuels index (series hfl_w1_pdmi_nn) is embedded in the CPB WTM Excel file; it is also available directly from https://www.hwwi.org/en/data-offers/commodity-price-index/. No proprietary data are used; the analysis is fully replicable from publicly available sources.

A9.3 Replication Prompt

The following prompt may be used with an AI coding assistant to replicate the full analysis:

Using the CPB World Trade Monitor February 2026 Excel file (downloadable from https://www.cpb.nl/en/world-trade-monitor), replicate the analysis in Evenett (2026). The file contains two sheets: trade_out and inpro_out. Load: world trade volume (tgz_w1_qnmi_sn); HWWI Fuels index (hfl_w1_pdmi_nn); world industrial production (ipz_w1_qnmi_sm); 14 regional export series (xgz_[w1/i1/e6/us/gb/jp/a3/r2/d1/cn/a5/t1/l1/f3]_qnmi_sn). All series run January 2000 to February 2026 (314 observations, base year 2021=100). Construct: (1) log of the 12-month rolling standard deviation of monthly log fuel price changes multiplied by 100, as the volatility regressor; (2) log of the HWWI Fuels index shifted forward Y months, as the level regressor; (3) residual from regressing the Y-month percentage change in world industrial production on regressors (1) and (2), as the purged IP control. For each dependent series and for Y in {6,7,...,24}: compute dependent as 100*(series[t+Y]-series[t])/series[t]; estimate OLS with HAC standard errors (Newey-West, maxlags=Y); record AIC, BIC, R2, and for each coefficient: estimate, SE(OLS), t(OLS), p(OLS), SE(HAC), z(HAC), p(HAC), 95% CI(HAC). Identify optimal Y by AIC and by R2. Report full regression tables at both horizons. Compute Z = beta_vol * log(1.10). Apply 2% dep-var trim robustness check to all series at all Y. Produce: (1) dual-axis time series of fuel volatility and forward trade growth; (2) two-panel beta profiles across Y; (3) Z bar chart with confidence intervals; (4) ranked horizontal bar chart of Z at Y=19; (5) two-scenario projection chart.

A9.4 Python Replication Code

The full annotated Python code is provided below. It produces all results reported in the annex and all figures in the policy brief.

# ============================================================ # Evenett (2026) Replication Code # Oil Price Volatility, Energy Price Levels, and World Trade # Full annotated script # ============================================================ import pandas as pd import numpy as np from openpyxl import load_workbook import statsmodels.api as sm from scipy.stats import pearsonr import matplotlib matplotlib.use('Agg') import matplotlib.pyplot as plt import warnings warnings.filterwarnings('ignore') # ── Section 1: Load data ───────────────────────────────────── # Download the CPB WTM file from: # https://www.cpb.nl/en/world-trade-monitor FILE = "cpb-world-trade-monitor-february-2026.xlsx" wb = load_workbook(FILE, read_only=True) ws_t = wb["trade_out"] ws_i = wb["inpro_out"] rows_t = list(ws_t.iter_rows(values_only=True)) rows_i = list(ws_i.iter_rows(values_only=True)) # Parse dates from row 3 (0-indexed) header = rows_t[3] dates_raw = [c for c in header[5:] if c is not None] dates = [pd.Timestamp(year=int(s[:4]), month=int(s[5:]), day=1) for s in dates_raw] def get_series(rows, label, code): """Extract a named series from a WTM sheet.""" for r in rows: if r[1] == label and r[2] == code: return pd.Series( list(r[5:5+len(dates)]), index=dates, dtype=float) return None # ── Section 2: Construct regressors ───────────────────────── trade_vol = get_series(rows_t, 'World trade', 'tgz_w1_qnmi_sn') fuel_price = get_series(rows_t, 'Fuels (HWWI)', 'hfl_w1_pdmi_nn') indpro = get_series(rows_i, 'World', 'ipz_w1_qnmi_sm') log_fuel = np.log(fuel_price) # Fuel volatility: 12-month rolling SD of log fuel changes x100 fuel_std = log_fuel.diff().dropna() * 100 fuel_vol = fuel_std.rolling(12).std() # in pct terms log_fuel_std = np.log(fuel_vol) # log of volatility # delta_log for the "10% rise" calculation delta_log = np.log(1.10) # ── Section 3: Two-stage regression function ───────────────── def run_regression(dep_series, Y, trim_pct=None): """ Estimate the two-stage purged IP regression. Parameters ---------- dep_series : pd.Series Trade or export volume index (level, not log). Y : int Forecast horizon in months. trim_pct : float or None If not None, removes this fraction from each tail of the dependent variable. E.g. 0.02 for 2%. Returns ------- dict with keys: n, aic, bic, r2, b_vol, b_fl, b_ip, se_vol_hac, p_vol_hac, ci_lo, ci_hi, se_fl_hac, p_fl_hac, model, hac, df """ # Dependent variable: Y-month percentage change dep = dep_series.pct_change(periods=Y).shift(-Y) * 100 # Level regressor: log of fuel price at t+Y log_fuel_fwd = log_fuel.shift(-Y) # Stage 1: purge IP of fuel variables ip_pct = indpro.pct_change(periods=Y).shift(-Y) * 100 df_s1 = pd.DataFrame({ 'ip': ip_pct, 'fv': log_fuel_std, 'fl': log_fuel_fwd }).dropna() ip_purged = sm.OLS( df_s1['ip'], sm.add_constant(df_s1[['fv', 'fl']]) ).fit().resid # Stage 2: main regression df = pd.DataFrame({ 'dep': dep, 'fv': log_fuel_std, 'fl': log_fuel_fwd, 'ip': ip_purged }).dropna() # Apply trimming if requested if trim_pct is not None: lo = df['dep'].quantile(trim_pct) hi = df['dep'].quantile(1 - trim_pct) df = df[(df['dep'] >= lo) & (df['dep'] <= hi)] X = sm.add_constant(df[['fv', 'fl', 'ip']]) m_ols = sm.OLS(df['dep'], X).fit() m_hac = sm.OLS(df['dep'], X).fit( cov_type='HAC', cov_kwds={'maxlags': Y}) return { 'n': len(df), 'aic': m_ols.aic, 'bic': m_ols.bic, 'r2': m_ols.rsquared, 'b_vol': m_ols.params['fv'], 'b_fl': m_ols.params['fl'], 'b_ip': m_ols.params['ip'], 'se_vol_hac': m_hac.bse['fv'], 'p_vol_hac': m_hac.pvalues['fv'], 'ci_lo': m_hac.conf_int().loc['fv', 0], 'ci_hi': m_hac.conf_int().loc['fv', 1], 'se_fl_hac': m_hac.bse['fl'], 'p_fl_hac': m_hac.pvalues['fl'], 'model': m_ols, 'hac': m_hac, 'df': df } # ── Section 4: Grid search Y = 6..24 for all series ───────── export_series = { 'World': ('World exports', 'xgz_w1_qnmi_sn'), 'Advanced economies': (' Advanced economies', 'xgz_i1_qnmi_sn'), 'Euro Area': (' Euro Area', 'xgz_e6_qnmi_sn'), 'United States': (' United States', 'xgz_us_qnmi_sn'), 'United Kingdom': (' United Kingdom', 'xgz_gb_qnmi_sn'), 'Japan': (' Japan', 'xgz_jp_qnmi_sn'), 'Adv Asia ex Japan': (' Advanced Asia excl Japan','xgz_a3_qnmi_sn'), 'Other advanced': (' Other advanced economies','xgz_r2_qnmi_sn'), 'Emerging economies': (' Emerging economies', 'xgz_d1_qnmi_sn'), 'China': (' China', 'xgz_cn_qnmi_sn'), 'Emerg Asia ex China': (' Emerging Asia excl China','xgz_a5_qnmi_sn'), 'Eastern Europe/CIS': (' Eastern Europe / CIS', 'xgz_t1_qnmi_sn'), 'Latin America': (' Latin America', 'xgz_l1_qnmi_sn'), 'Africa & Middle East':(' Africa and Middle East', 'xgz_f3_qnmi_sn'), } all_results = {} all_trimmed = {} for region, (label, code) in export_series.items(): ev = get_series(rows_t, label, code) all_results[region] = {} all_trimmed[region] = {} for Y in range(6, 25): all_results[region][Y] = run_regression(ev, Y) all_trimmed[region][Y] = run_regression(ev, Y, trim_pct=0.02) # Also run for world trade volume (not exports) world_results = {} world_trimmed = {} for Y in range(6, 25): world_results[Y] = run_regression(trade_vol, Y) world_trimmed[Y] = run_regression(trade_vol, Y, trim_pct=0.02) # ── Section 5: Key output tables ──────────────────────────── print("Grid search results: world trade volume") print(f"{'Y':>3} {'n':>4} {'AIC':>9} {'BIC':>9} {'R2':>7} " f"{'b_vol':>8} {'p_hac':>8} {'b_fl':>8} {'b_ip':>8}") for Y in range(6, 25): r = world_results[Y] Z = r['b_vol'] * delta_log print(f"{Y:>3} {r['n']:>4} {r['aic']:>9.1f} {r['bic']:>9.1f} " f"{r['r2']:>7.4f} {r['b_vol']:>8.3f} " f"{r['p_vol_hac']:>8.4f} {r['b_fl']:>8.3f} {r['b_ip']:>8.3f}") # ── Section 6: Print full regression at Y=6 and Y=19 ──────── for Y_print in [6, 19]: r = world_results[Y_print] print(f"\n=== Full regression Y={Y_print} ===") print(r['model'].summary()) print("\nHAC standard errors:") print(r['hac'].summary()) # ── Section 7: Regional Z at Y=19 ──────────────────────────── print("\nZ statistics at Y=19 (pp per 10% rise in fuel vol):") for region in export_series: r = all_results[region][19] Z = r['b_vol'] * delta_log print(f" {region:<25}: Z={Z:.3f} p(HAC)={r['p_vol_hac']:.3f}") # ── Section 8: Robustness check summary ───────────────────── print("\nRobustness: 2% trim vs baseline at Y=19") for region in list(export_series.keys()) + ['World trade']: src = world_results if region=='World trade' else all_results[region] trm = world_trimmed if region=='World trade' else all_trimmed[region] Zb = src[19]['b_vol'] * delta_log Zt = trm[19]['b_vol'] * delta_log pb = src[19]['p_vol_hac'] pt = trm[19]['p_vol_hac'] flip = '*** FLIPS' if (pb<0.05)!=(pt<0.05) else '' print(f" {region:<25}: Zbase={Zb:.3f} p={pb:.3f} | " f"Ztrim={Zt:.3f} p={pt:.3f} {flip}") # ── Section 9: Figures ──────────────────────────────────────── # See the policy brief for figure descriptions. # Chart generation code follows the structure used in the # original analysis. Colours: C_FUEL='#c0392b', C_TRADE='#1a5fa8' # All charts saved as PNG at 150 DPI. print("\nAll results computed. Generate charts as per policy brief.")

The code above is complete and self-contained. Running it with the CPB WTM February 2026 Excel file will reproduce all tables and key statistics reported in this annex. Chart generation code follows the structure established in the analysis session from which this paper derives and is available from the author on request in full annotated form.

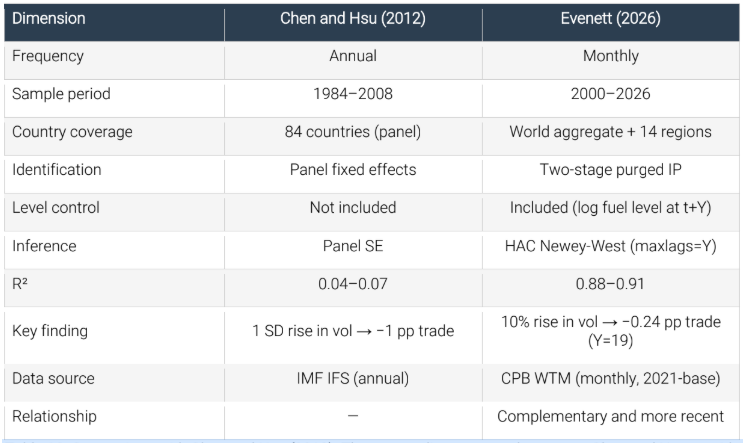

A9.5 Comparison with Chen and Hsu (2012)

Table A9: Comparison with Chen and Hsu (2012). The two studies are complementary: Chen and Hsu provide a broad cross-country foundation; the present study extends their finding to a more recent period with a more demanding specification.

References in the Technical Annex

Berlemann, M., Eurich, M. and Meyer, H. (2023). HWWI Commodity Price Index: A Technical Documentation of the 2023 Revision. HWWI Working Paper No. 1/2023. Hamburg: Hamburg Institute of International Economics.

Chen, S.-S. and Hsu, K.-W. (2012). Reverse globalization: Does high oil price volatility discourage international trade? Energy Economics, 34(5), 1634–1643.

Ebregt, J., Hendriks, B. and Ligthart, M. (2024). The CPB World Trade Monitor: Technical Description. CPB Background Document, July 2024. The Hague: CPB Netherlands Bureau for Economic Policy Analysis.

Hendriks, B. and Ligthart, M. (2024). Technical Changes to WTM: Change of Base Year, Seasonal Correction Procedure and Underlying Data Sources. CPB Memo, 25 July 2024. The Hague: CPB Netherlands Bureau for Economic Policy Analysis.

Jordà, O. (2005). Estimation and inference of impulse responses by local projections. American Economic Review, 95(1), 161–182.

Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review, 99(3), 1053–1069.

Newey, W.K. and West, K.D. (1987). A simple, positive semi-definite, heteroscedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3), 703–708.

1

Professor of Geopolitics & Strategy, IMD Business School; Founder, St. Gallen Endowment for Prosperity Through Trade; and Co-Chair, World Economic Forum Trade & Investment Council. Email address: simon.evenett@imd.org. The empirical analysis was conducted with assistance from Claude (Anthropic). All errors remain the author’s own.

2

Chen and Hsu’s paper has been cited 130 times.

3

Data constraints preclude examining the effects on services trade and cross-border digitally delivered services.

4

This index is published monthly in US dollars and is available at https://www.hwwi.org/en/data-offers/commodity-price-index/.

5

A priori, I do not know how long it takes for fuel prices to affect trade volumes, so I let the data reveal which forward horizon has the greatest explanatory power.

6

A 19 month forward interval was found to maximise the explanatory power of the two-stage regression performed on world trade volumes.

7

Econometric details are explained at length in the technical annex to this paper.

8

Regrettably, the World Trade Monitor does not publish separate data for certain well-used groupings of developing countries, such as the Least Developed Countries.

9

Such an export hit would compound any Gulf conflict-related food price volatility that has rightly received attention in recent weeks.

10

The latest available WTM excel file has 13 distinct major economies or country groupings below the world aggregate. The WTM background documentation mentions 14 groups, which may be an error.