What intermediated support is

Financial intermediation occurs when governments enable banks or funds to deploy capital on their behalf. These intermediaries can be private or public. The distinctive feature: the intermediaries have no direct fiscal or institutional tie to the government agency providing the support. This institutional layer separates state capital from its final recipient.

The Global Trade Alert taxonomy distinguishes between two different instruments. Lending support captures financial backing that enables corporate credit access: a development bank provides capital to a commercial bank, which lends it onward to businesses. Financial investment support captures backing to intermediary funds that invest in companies, typically through equity stakes or capital injections. The two instruments differ in their sectoral targeting rates and in the detail observable in the data.

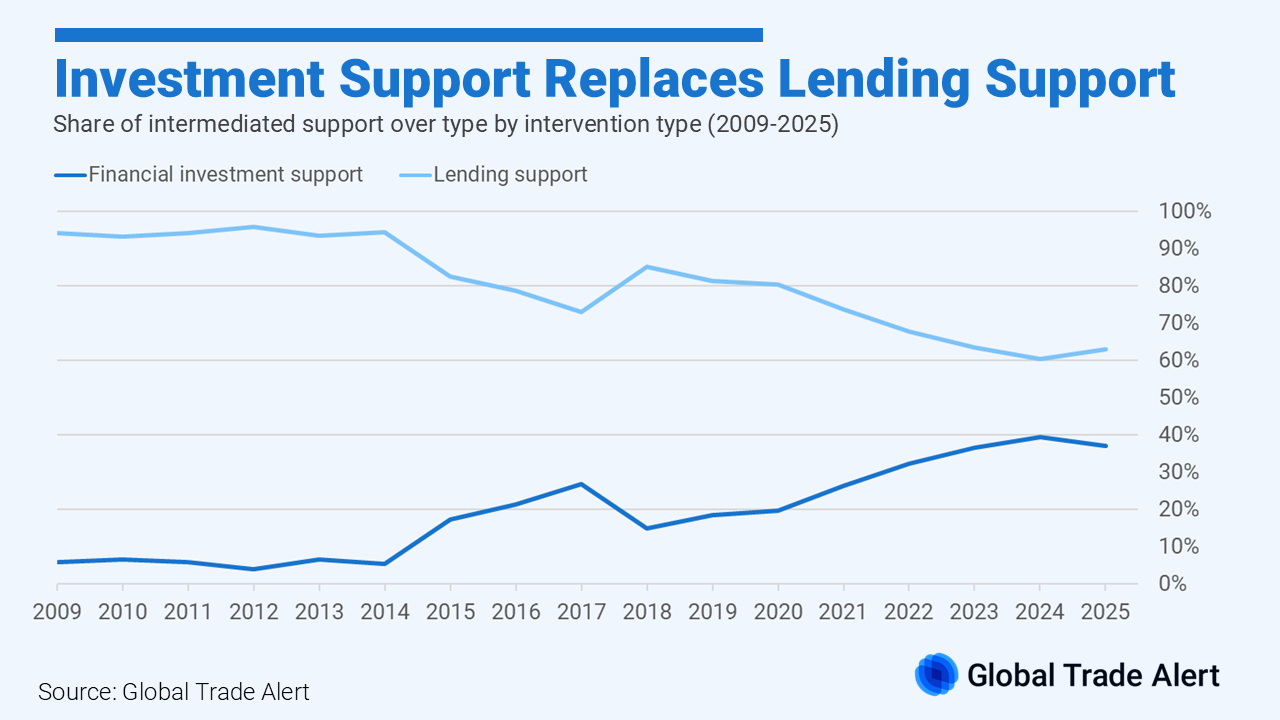

The shift from lending to investment

The composition of documented intermediated support has changed substantially since 2009. Between 2009 and 2014, lending support made up 93 to 96 per cent of recorded interventions. By 2024, lending’s share had fallen to 60 per cent, with investment-based support rising to 40 per cent. The inflexion began around 2015 and accelerated after 2020. Average annual interventions rose from 6 (2009 to 2014) to 58 (2020 to 2025).

Sectoral targeting has increased alongside the shift to investment instruments. From 2009 to 2025, 62% of interventions applied horizontally across all sectors; in 2025, sector-specific interventions comprised 85% of recorded measures. However, financial investment support measures are nearly three times more likely to target specific sectors than lending support measures: 75% versus 28% across the full dataset. By 2025, sectoral targeting reached 79% for lending support and 95% for financial investment support, though these figures rest on a single year’s recorded interventions.

The 2009 to 2014 baseline coincides with the global financial crisis, when governments deployed broad, horizontal measures to stabilise credit markets. The inflexion around 2015 also coincides with expanded GTA coverage of equity-type instruments. The available data do not isolate how much of the subsequent shift reflects actual policy change, how much reflects the natural unwinding of crisis-era measures, how much reflects improved monitoring of investment instruments, and how much reflects other factors, including regulatory changes (Basel III and IV), the low interest rate environment, or the design of specific programmes such as the European Fund for Strategic Investments and InvestEU.

What this looks like in practice

The European Investment Bank (EIB) and Nordic Investment Bank (NIB) transaction structure is well-documented. EIB and NIB account for 90% of all recorded European interventions. The EU member states represent 74% of documented intermediated support globally. For example, in November 2019, the European Investment Bank provided USD 110 million to Banco BPM SpA, a private Italian bank, to support agricultural small and medium enterprises. The intermediary is identified, the sector is specified, and the amount is public. What is not observable is which agricultural SMEs received capital, on what terms, or whether the allocation achieved its stated objectives.

Chinese guidance funds operate with less transparency and more institutional layers. These are public-private investment vehicles that deploy through equity investments and capital injections. Some invest directly in companies: a USD 6 billion fund for emerging industries launched in 2016 illustrates this model. Others operate through fund-of-funds structures that invest in sub-funds, which then invest in businesses: the USD 21.8 billion Industry Investment Fund of Funds is one example. The number of institutional layers between governmental capital and the receiving firm can be large.

What the data can and cannot tell us

Intermediary identification rates have declined sharply. Between 2009 and 2014, intermediaries were identified in 87% of recorded interventions. Between 2020 and 2025, that figure fell to 39%. The expansion of the dataset to jurisdictions with lower systematic disclosure would mechanically reduce the average. Changes in reporting formats and in disclosure practices by implementing governments may also contribute. The data do not isolate which factor is dominant.

China’s 118 recorded interventions understate actual activity. Guidance funds operate at a scale that exceeds monitoring capacity. As of early 2020, a Centre for Security and Emerging Technology research identified 1,741 guidance funds in total, the majority established at the municipal and county level. Most lack public documentation of the kind that systematic monitoring requires.