Subsidising the Chokepoint: Strategic Convergence and Its Limits

ZEITGEIST SERIES BRIEFING #88

ZEITGEIST SERIES BRIEFING #88

Fernando Martín Espejo

01 Apr 2026

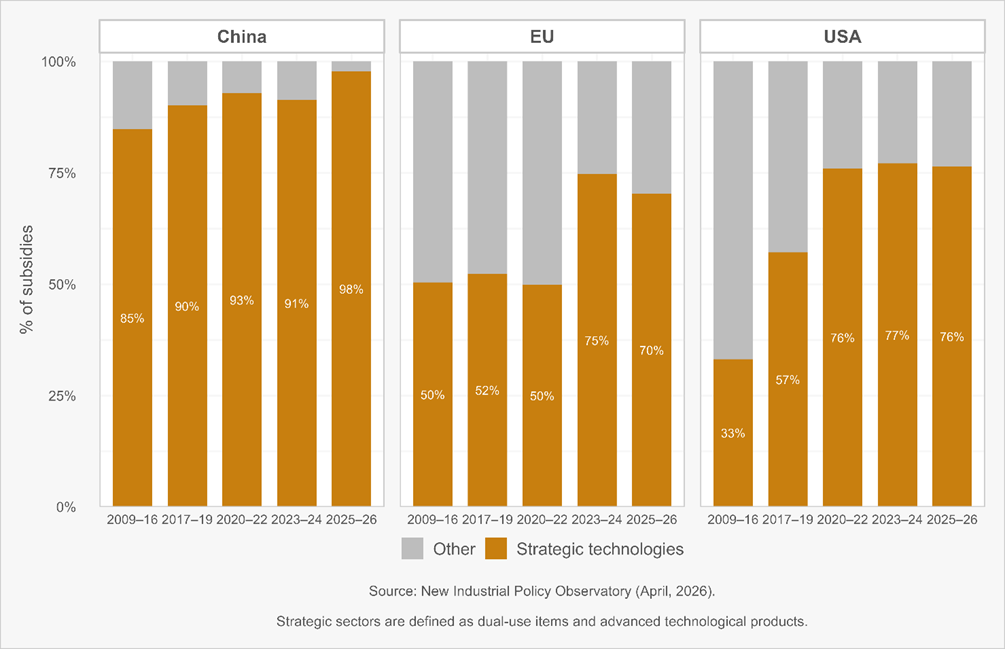

Figure 1 tracks the share of subsidy-based industrial actions covering at least one dual-use item or advanced technology product across the three jurisdictions, using data from the New Industrial Policy Observatory (NIPO). The pattern is clear: in 2009–16, China already directed 85% of its subsidy activity toward strategic technologies; the EU stood at 50% and the United States at just 33%. By 2025–26, China reaches 98%, the EU 70%, and the US 76%. All three blocs have converged on targeting the same chokepoints (semiconductors, critical minerals, batteries, advanced electronics) but they arrived through very different paths and at very different speeds.

China's strategic targeting goes back to the beginning of the dataset. The Strategic Emerging Industries programme (2010) designated seven priority sectors; Made in China 2025 (2015) set explicit domestic-content targets for core components. The National IC Industry Investment Fund ("Big Fund") committed ¥138.7 billion in Phase I (2014), ¥204.1 billion in Phase II (2019), and ¥344 billion in Phase III (2024) with a cumulative direct capital of approximately ¥687 billion (~$98 billion) for semiconductors alone. Figure 1 confirms that this architecture was already operational early: strategic sectors absorbed 85% of Chinese subsidy actions in 2009–16 and never fell below 90% thereafter. The 15th Five-Year Plan (2026–30) reinforces this trajectory, reaffirming the strategic importance of maintaining manufacturing scale in semiconductors, AI, and advanced manufacturing.

Crucially, China's subsidies were embedded within a broader ecosystem of state-directed credit, procurement preferences, and a large domestic market. But financial support alone does not explain the outcome. Research on China's clean-energy industries shows that rapid cost reduction was driven less by the subsidies themselves than by the speed of manufacturing scale-up, supply chain localisation, and intense competition among hundreds of domestic firms that forced continuous process innovation (Nahm & Steinfeld, 2014; Nahm, 2021). Where these complementary conditions were absent, as in semiconductors, massive state funding has produced far more modest results (Kennedy, 2024). The distinction matters: China's strategic industrial policy succeeded because financial support was layered onto domestic competition, integrated value chains, and a large internal market that together created self-reinforcing dynamics.

The US transformation is the most dramatic. From a baseline of 33% in 2009–16, strategic-sector targeting jumped to 57% in 2017–19, coinciding with Section 301 tariffs, Entity List designations (Huawei, May 2019), and the first wave of semiconductor export controls. The CHIPS and Science Act and the Inflation Reduction Act (August 2022) cemented the shift. By 2020–22, 76% of US subsidy actions targeted strategic sectors, stabilising near that level through 2025–26. The October 2022 advanced semiconductor export controls, restricting chips above 300 TOPS and EUV lithography equipment destined for China, added a chokepoint dimension that complemented domestic subsidies with technology denial. An Executive Order on outbound investment screening (August 2023) completed the architecture by restricting US capital flows into Chinese semiconductors, quantum, and AI.

The EU's trajectory is the most compressed. Through 2020–22, strategic-sector subsidies remained at or below 50%. The break came after COVID-19, the semiconductor shortage, Russia's invasion of Ukraine, and, most catalytically, the US Inflation Reduction Act, which was seen as a threat to redirect clean-tech investment across the Atlantic. The EU responded with the European Chips Act (September 2023, targeting €43 billion in mobilised investment), the Critical Raw Materials Act (May 2024), the Net-Zero Industry Act (June 2024), and multiple IPCEIs channelling over €37 billion in approved state aid into microelectronics, batteries, and hydrogen. As Figure 1 shows, the strategic share surged to 75% in 2023–24 before settling at 70% in 2025–26. The EU also expanded its defensive toolkit with the Foreign Subsidies Regulation and the Anti-Coercion Instrument.

The convergence in subsidy targeting is not the same as convergence in industrial capability. Recent experience suggests that financial support, however large, cannot by itself replicate the ecosystems that decades of sustained investment have built. Intel officially cancelled its €30 billion Magdeburg megafab in July 2025, a project for which the German government had pledged nearly €10 billion in state aid.[1] A €4.6 billion assembly facility near Wrocław, Poland, was cancelled alongside it. In the United States, Intel's Ohio fabs (originally slated for 2025 production) have been pushed to 2030–31, despite $7.86 billion in CHIPS Act grants.[2] These were flagship projects at the centre of each jurisdiction's semiconductor strategy.

The pattern suggests a structural mismatch: subsidies can attract announcements, but building a competitive fabrication ecosystem requires aligned demand, a deep supplier base, workforce pipelines, and sustained political commitment over business cycles. These are conditions that China's decade-long approach more closely approximates. Multi-year legislative commitments (CHIPS Act, IRA, Big Fund III, European Chips Act) lock in subsidy flows, but turning financial support into durable competitive advantage will require far more than the cheques themselves.

Kennedy, S. (2024, November 19). Wins and losses: Chinese industrial policy's uneven success. Center for Strategic and Industrial Studies, Big Data China. https://bigdatachina.csis.org/wins-and-losses-chinese-industrial-policys-uneven-success/

Martín, F. (2026). Industrial policy as market-shaping competition: Evidence from China, the European Union, and the United States (2009–2024). SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6143206

Nahm, J. (2021). Collaborative advantage: Forging green industries in the new global economy. Oxford University Press. https://doi.org/10.1093/oso/9780197555361.001.0001

Nahm, J., & Steinfeld, E. S. (2014). Scale-up nation: China's specialization in innovative manufacturing. World Development, 54, 288–300. https://doi.org/10.1016/j.worlddev.2013.09.003

Fernando Martín is Associate Director at Global Trade Alert, leading the Analytics team, and Geopolitical Strategist at IMD.