How often do China, the EU-27, and the United States retaliate against foreign industrial subsidies through trade defence instruments, tariffs, and import barriers? Using product-level data for the period 6, 12, and 24 months after a foreign subsidy is awarded, I find distinct national responses. Retaliatory steps increasingly concentrate on the so-called green and high-tech sectors, with tariffs dominating. Despite growing reliance on opaque tools, the continued use of trade remedies and shared sectoral focus suggest partial adherence to multilateral norms and potential pathways for future initiatives to unwind trade restrictions.

Authors

Fernando Martín Espejo

Date Published

06 Aug 2025

Related Topics:

The resurgence of industrial policy—via subsidies, tax incentives, and other state support—has reconfigured global trade policy dynamics. These subsidies prompt defensive responses from affected trading partners. G20 economies increasingly deploy a broad array of trade instruments—including trade defence measures, tariffs, and opaque import barriers—to counter foreign subsidies deemed trade-distorting.

This piece investigates whether, how, and when China, the EU-27, and the United States retaliate against such subsidies, based on product-level responses observed within 6, 12, and 24 months of the implementation of a subsidy. I draw upon the massive inventory of corporate subsidies assembled by the Global Trade Alert team. This analysis covers corporate subsidies awarded from 2017 to 2025.

Instrument Hierarchy and Strategic Preferences

Table 1 reveals distinct institutional preferences across actors for specific tools[1]:

-

China: Nearly 48% of China’s responses are opaque import barriers, and 36.2% are tariffs. Trade defence is used in only 15.9% of cases—suggesting a preference for WTO-risk-averse, flexible instruments likely to evade formal dispute settlement channels.

-

EU-27: Over 50% of EU responses are trade defence actions (e.g., anti-dumping, countervailing duties), reflecting a rule-based, WTO-consistent strategy. The EU’s preference aligns with its legalistic trade culture, WTO dispute settlement reliance (e.g., EU – Biodiesel (Argentina)), and sectoral lobbying pressures.

-

United States: The US splits its retaliation between trade defence (49.3%) and tariffs (45.2%), leveraging both legal channels (CVD/AD) and discretionary powers under Section 301 and national security exceptions (e.g., US – Steel and Aluminium, DS544). This duality reflects its hybrid legal-political approach to retaliation.

Temporal Response Patterns

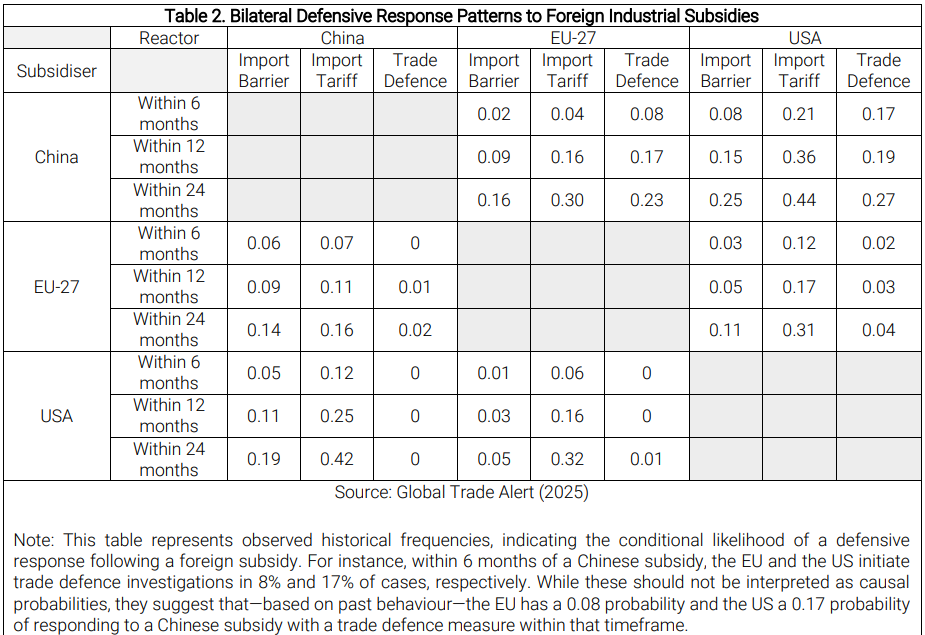

Table 2 presents the responses of China, the EU-27, and the United States to foreign subsidies—specifically in the form of import barriers, import tariffs, or trade defence investigations—tracked over 6-, 12-, and 24-month periods. This analysis covers all combinations of country-pairs, time horizons, and policy instruments:

-

EU responses to Chinese subsidies are quicker and more legalistic. Within 6 months, the EU initiates trade defence cases against 8% of Chinese subsidies—compared to just 2% through import barriers and 4% via tariffs. This trend continues at 12 months, with 17% of Chinese subsidies met by EU trade defence measures. However, by 24 months, EU retaliation shifts: 30% of Chinese subsidies are matched with an import tariff, suggesting a gradual move toward broader instruments over time.

-

The US retaliates against Chinese subsidies more rapidly and across a broader set of tools. Within 6 months, US tariffs are applied in 21% of cases, slightly outpacing trade defence (17%). By 24 months, tariffs respond to 44% of Chinese subsidies, and import barriers to 25%, indicating a heavy reliance on flexible and immediate instruments.

-

China predominantly uses import barriers and tariffs—especially against US subsidies. Within 24 months, China responds to 42% of US subsidies with a tariff increase, compared to just 16% of EU subsidies. Trade defence is rarely used by China in retaliatory fashion.

-

Transatlantic retaliation is dominated by import tariffs. The US reacts more swiftly than the EU: within 6 months of an EU subsidy, the US imposes tariffs in 12% of cases, compared to the EU’s 6% response rate to US subsidies. Yet by 24 months, the EU’s cumulative tariff response to US subsidies reaches 32%, slightly exceeding the US’s 31% response. The US also employs import barriers more frequently than the EU and makes marginally greater use of trade defence against the EU, though such cases remain infrequent overall.

Sectoral Patterns of Retaliation

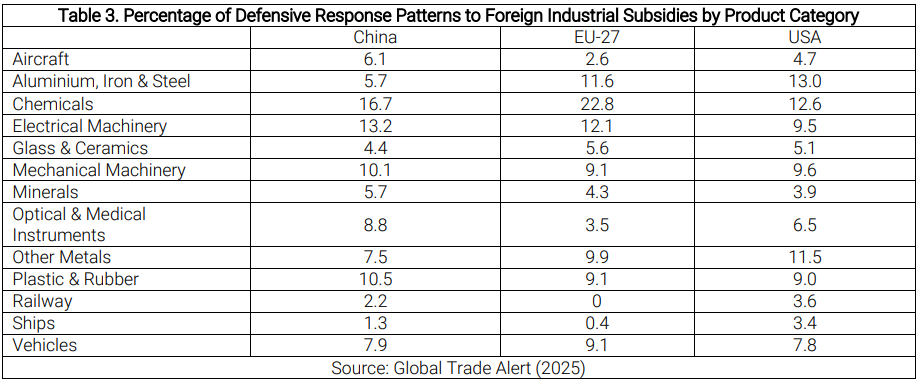

Table 3 shows strong targeting convergence on sectors central to high-tech and green industrial transitions:

-

Chemicals are the top target across all actors (EU: 22.8%, China: 16.7%, US: 12.6%), followed by machinery, vehicles, and plastics.

-

Aircraft and ships, despite high political visibility, are rarely retaliated against—likely due to legal sensitivity (e.g., EU – Airbus and US – Boeing disputes) and the complexity of global supply chains.

Key Insights

-

The EU, US, and China adopt distinct defensive strategies against foreign subsidies. The EU tend to rely on WTO-compliant trade defence tools, the US balances trade defence with politically driven tariffs, and China favours opaque import restrictions. These preferences reflect institutional norms and domestic politics but also signal diverging commitments to WTO legality.

-

Retaliatory actions intensify over time, with tariffs becoming the dominant tool by 24 months. The EU responds to Chinese subsidies with trade defence more frequently early on, while the US reacts faster and more aggressively with tariffs. Both actors increasingly substitute tariffs for legal remedies as WTO enforcement weakens.

-

Retaliation concentrates on green and high-tech sectors—like chemicals, machinery, and vehicles—rather than traditional industries, reflecting strategic targeting of sensitive, high-value areas.

-

Structural shifts are also evident: rising use of non-transparent tools, reduced legal enforceability due to the Appellate Body’s paralysis, and persistent but uneven adherence to WTO norms. Converging sectoral focus may signal opportunities for future coordination or managed retaliation frameworks.

Retaliation in Context: What Lies Ahead

The global trade system is being reshaped by the rise of industrial policy and a weakening of WTO enforcement. While the EU, US, and China differ in how they retaliate, their shared turn to tariffs and informal barriers reflects fading confidence in WTO rules on subsidies. Yet the limited rate of direct responses to subsidies suggests that not all are viewed as threatening, raising questions about which interventions truly warrant global concern.

Despite rising tensions, the concentration of responses in strategic sectors shows that some multilateral norms still guide behaviour. Moving forward, managing trade frictions will require updated WTO rules and stronger coordination—not just legal confrontation. For corporate leaders, this means preparing for more politicised trade policy, sector-specific risks, and greater regulatory fragmentation. Engagement with policymakers will be critical to navigate the shifting landscape.

Fernando Martín is an Associate Director at the Global Trade Alert leading the Analytics team.

1

Table 1 reports the percentages of responses by China, the EU-27, and the United States that occur within 24 months of a foreign subsidy’s implementation, expressed as a percentage of their total responses.